Written by : Alen Vi | Creditcardviews.com

Meet Alex. Alex is a sophomore at a major U.S. university. Like millions of other students, Alex doesn’t have a traditional 9-to-5 job. Between 15-credit semesters, grueling lab reports, and club meetings, there just isn’t time for a “paycheck.”

But last week, Alex’s car broke down. Then, Alex tried to apply for an off-campus apartment, only to be told: “Sorry, you have no credit history.”

It’s the ultimate Catch-22: You need credit to get an apartment, but you can’t get credit because you don’t have a “job.” If you’ve felt that pit in your stomach—the fear that you’re falling behind financially before your life even starts—you aren’t alone.

Here is the good news: In 2026, you do not need a traditional job to get a credit card. In this comprehensive guide, we will break down exactly how student credit card no income USA strategies work. We’ll show you how to navigate the legal loopholes, which banks are the most student-friendly, and how to build credit without income USA starting today.

1. Why Students Need a Credit Card in the U.S. (More Than Ever)

In 2026, a credit score is more than just a number for a loan; it is your “financial resume.” Whether you are a domestic student or an international student, your credit history impacts your quality of life more than you might realize.

The Real-World Stakes

- Housing and Independence: According to the Consumer Financial Protection Bureau’s (CFPB) 2025 Consumer Credit Card Market Report, credit visibility is a primary barrier to entry for young renters. Most landlords in major hubs like New York, Chicago, or Los Angeles won’t even show you an apartment without a credit check.

- Security Deposits: Having a high credit score can waive hundreds of dollars in deposits for utilities (electricity, water) and cell phone plans. For a student on a budget, that $200 utility deposit could be better spent on textbooks or groceries.

- Employment Screening: Believe it or not, some employers in the financial, legal, or government sectors run credit checks during the background check process to assess your “financial responsibility.”

- Emergency Safety Net: Life happens. A credit card provides a buffer for medical emergencies, last-minute travel, or car repairs when your bank account is low.

The Data Proof:

According to the Federal Reserve’s 2025 Report on the Economic Well-Being of U.S. Households in 2024, only 66% of adults aged 18 to 29 reported “doing okay” financially—a significantly lower rate than older cohorts. This suggests that younger consumers are under more pressure than ever to build financial buffers. Furthermore, the report highlights that credit card fraud is the most common type of financial crime, and holding your own account with a major bank provides significantly better fraud protection than debit cards or cash.

If you wait until you graduate to start building credit, you are already four years behind your peers.

2. Can You Get a Credit Card Without Income? The Legal Truth

Many students ask: “Is it even legal to get a credit card if I’m not working?” The answer is a resounding YES, but there is a nuance you must understand regarding how banks evaluate your “Ability to Pay.”

The “Ability to Pay” Rule

The Credit CARD Act of 2009 and the Equal Credit Opportunity Act (ECOA) set the rules. By law, a bank cannot give you a credit card unless they believe you have the “ability to pay” the bill.

- If you are under 21: The rules are stricter. You must show “independent” income or have a co-signer (though most big banks no longer allow co-signers).

- If you are 21 or older: You can legally include any income to which you have a “reasonable expectation of access.” This includes a spouse’s or partner’s income.

Mentor Tip: Banks don’t care if you have a “boss.” They care if you have “accessible funds.”

What Counts as Income for Students in 2026?

When you see the “Total Gross Annual Income” box on an application, you are not lying by including these sources. In fact, under current consumer protection guidelines, these are valid forms of income:

- Scholarships & Grants: Any money left over after tuition and fees are paid.

- Parental/Family Allowances: Regular deposits made into your account by family.

- Personal Savings: Money you’ve saved from summer jobs, internships, or graduation gifts.

- Financial Aid: The “refund check” you receive from the school for living expenses.

- Side Hustles: Income from tutoring, DoorDash, Etsy, or freelance coding.

Quick Strategy to Ensure Approval

Even without a “job,” you should never put $0 in the income box. To pass the “Ability to Pay” check used by banks in 2026, make sure to include:

- Financial Aid Refunds: The money sent to you after tuition is paid.

- Family Allowances: Any money parents or relatives send you for rent/food.

- Scholarships/Grants: Total annual value of non-loan financial awards.

- Side Hustles: Income from tutoring, gig work, or selling items online.

⚠️ A Note on the “Chase $250 Rule”: If you are eyeing the Chase Freedom Rise, the 2026 data shows that having at least $250 in a linked Chase checking account for just 3-5 days before applying significantly increases your approval odds.

🚀 The Student Credit Card Application Checklist

Before you click “Apply,” make sure you have checked off these 5 critical items to maximize your approval odds:

- [ ] Calculate Your “Real” Income: Total up your scholarships (the refund portion), monthly family allowance, and any side-hustle money. Never put $0.

- [ ] Gather Your Digital Documents: Have a PDF or clear photo of your Student ID and your current semester enrollment verification (or transcript) ready to upload.

- [ ] Check Your Bank Balance: If applying for a “Relationship Bank” like Chase, ensure you have at least $250 in your checking account to trigger their internal approval AI.

- [ ] Pick One Card (For Now): Do not “shotgun” apply to 5 cards at once. Pick the one from the chart above that best fits your needs to avoid multiple hard hits to your credit score.

- [ ] Set a “Safety” Reminder: Once approved, immediately set a calendar alert for your first payment date. One late payment in your first 6 months can stall your credit growth for years.

2026 Student Credit Card Comparison: No Income Required

3. Types of Credit Cards for Students (2026 Rankings)

Choosing the right card is the difference between a quick approval and a “Hard Inquiry” that leaves you with a rejected application. Based on 2026 underwriting trends, these cards offer the highest approval odds for students using scholarships, grants, and allowances as income. Find your match and apply in under 5 minutes.

| Card Name | Best For | Key Benefits | Deposit? | Apply Link |

| Discover it® Student Cash Back | Overall Best | 5% Rotating Cash Back + First Year Match | No | Apply Now |

| Chase Freedom Rise℠ | Bank Account Holders | 1.5% Flat Cash Back; Odds higher with $250 in bank | No | Apply Now |

| Capital One SavorOne Student | Foodies & Dining | 3% Back on Dining, Groceries, & Streaming | No | Apply Now |

| BofA Customized Cash (Student) | International Students | 3% Back in a category of your choice; No SSN needed | No | Apply Now |

| OpenSky® Secured Visa® | Guaranteed Approval | No Credit Check; 89% Approval Rate | Yes ($200+) | Apply Now |

⚖️ Legal Disclaimer (Place at bottom of chart)

Note: While the strategies in this guide are based on 2026 financial regulations and bank policies, credit card approval is never 100% guaranteed. All applicants must be at least 18 years old. Always read the “Terms and Conditions” and the “Schumer Box” (Interest Rates & Fees) provided by the bank before signing. This guide is for educational purposes and does not constitute professional financial advice.

📊 Visualizing Your Odds: 2026 Approval Comparison

Based on current 2026 underwriting trends, here is how the primary card types compare for a student with no traditional income:

Approval Odds by Card Type (2026)

Secured Cards ████████████████████ 95%

Student Cards ██████████████ 70%

Cash-Flow Cards █████████████ 65%

Standard Cards ████ 20%

Student-Specific Credit Cards

These are “unsecured” cards (no deposit required) designed for people with zero credit.

- Best for: Students with some form of verifiable allowance or scholarship.

- Pros: Build credit fast; earn rewards like cash back.

- Cons: Lower initial limits (usually $300 – $1,000).

Secured Credit Cards

You provide a refundable deposit (e.g., $200) which becomes your credit limit.

- Best for: Those who have been rejected for student cards or are starting from zero.

- Pros: Almost 100% approval rate.

- Cons: Your money is “locked” until you “graduate” to a regular card.

The Authorized User Strategy

A parent adds you to their existing credit card account. You don’t even have to use the card for this to work.

- Best for: Students with parents who have great credit.

- Pros: You “inherit” their long credit history instantly.

- Cons: If the parent misses a payment, your score drops too.

Cash-Flow Based Cards (The 2026 Trend)

In 2026, many fintechs use “Cash-Flow Underwriting.” They link to your bank account via Plaid to see how much money you keep in your balance rather than looking at a traditional credit score.

Comparison of Credit Card Types for Students (2026 Data)

| Card Type | Deposit Required? | Approval Difficulty | Best For |

| Student Unsecured | No | Medium | Students with allowances |

| Secured Card | Yes ($200+) | Very Low | Total beginners / Rebuilds |

| Authorized User | No | None (if parent agrees) | Quick score boost |

| Cash-Flow Card | No | Low | High bank balance, no job |

4. How to Get a Credit Card Without Income: The 2026 Step-by-Step Guide

Step 1: Audit Your “Income”

Before applying, calculate every dollar you receive. If your parents send you $400 a month for groceries and rent, that is $4,800/year. If you have a $2,000 scholarship refund, your total income is $6,800. Never put “$0” on an application. Banks interpret $0 as an automatic inability to pay.

Step 2: Check Your Credit Report (Even if it’s Empty)

Go to AnnualCreditReport.com. Sometimes identity theft or clerical errors occur. You want to ensure your report is a “blank slate” before you start.

Step 3: Use “Prequalification” Tools

Banks like Capital One and Discover allow you to see if you are likely to be approved without a “hard pull” on your credit. This protects your score from a 5-10 point drop.

Step 4: Open a College Checking Account First

Banks are 5x more likely to approve you if you already have a checking account with them. If you want a Chase card, open a Chase College Checking account three months before applying.

Step 5: The Application

Apply online. When asked for your “Employment Status,” select “Student.” This triggers the bank’s “Student Underwriting” model, which is much more lenient regarding income requirements.

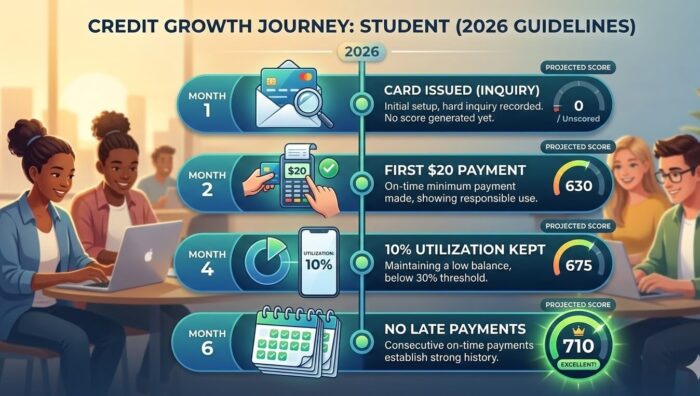

📉 The Impact of Responsibility (6-Month Score Projection)

If Alex follows the “Netflix & Autopay” strategy, here is the projected trajectory of his FICO score based on Experian’s 2026 Student Credit Benchmarks:

| Timeline | Activity | Projected Score |

| Month 1 | Card Issued (Inquiry) | 0 / Unscored |

| Month 2 | First $20 Payment | 630 |

| Month 4 | 10% Utilization Kept | 675 |

| Month 6 | No Late Payments | 710 |

5. Major U.S. Banks: Their 2026 Student Policies & Walkthroughs

In 2026, the “Big Four” banks have shifted toward Cash-Flow Underwriting. Here is how to navigate the application process for the top contenders.

Chase: The “Relationship First” Path

Chase is notoriously picky, but they launched the Chase Freedom Rise℠ specifically for those with zero credit.

- The “Secret Sauce”: The $250 Rule. Chase’s internal systems look for a $250 balance in a linked Chase checking account. If it’s there for at least 3 days before you apply, your approval odds skyrocket.

- 2026 Update: Chase now offers a $25 statement credit just for setting up Autopay within the first three months.

Discover: The “Student Standard”

Discover remains the most beginner-friendly major issuer. The Discover it® Student Cash Back is famous for its “Cashback Match,” where they double all rewards in your first year.

- The “Good Grades” Bonus: In 2026, Discover continues to offer a $20 statement credit each school year your GPA is 3.0 or higher (for up to 5 years).

- Application Tip: Have your .edu email or a digital copy of your transcript ready to verify enrollment.

Capital One: The “No-Risk Prequalifier”

Capital One’s SavorOne Student card is the 2026 favorite for foodies and streamers (3% back on dining and grocery stores).

- 2026 Tech: Capital One now integrates with Plaid. If you choose to “Link Your Bank,” their AI can approve you based on your savings balance even if your credit report is a total blank.

Bank of America: The “International Haven”

For students without a Social Security Number (SSN), Bank of America is the “Gold Standard.”

- The “No SSN” Strategy: They accept the Form I-20 and a foreign passport as primary identification.

- In-Person Advantage: Unlike other banks, BofA prefers international students to apply at a physical branch. Schedule an appointment online to meet with a representative.

American Express: The “Global Shortcut”

In 2026, Amex uses Nova Credit technology to “pull” your credit history from your home country (India, Mexico, UK, etc.) and apply it to a U.S. application.

6. The International Student Challenge (No SSN)

If you are an international student, the lack of a Social Security Number (SSN) is a hurdle, but not a wall. Use these 2026 strategies:

- Apply for an ITIN: An Individual Taxpayer Identification Number can often be used in place of an SSN for credit applications.

- Passport-Based Applications: As mentioned, Bank of America and Amex have specific programs allowing you to use your passport.

- Alternative Fintechs: Companies like Deserve or Petal specialize in “Alternative Data” and often approve students based on their education and bank balances rather than an SSN-linked credit score.

7 . 20 Actionable Tips to Guarantee Approval & Build Credit Fast

- The $250 Rule: Keep at least $250 in your bank account for 90 days before applying.

- Avoid “Credit Shopping”: Don’t apply for 5 cards in one week. It looks desperate to banks.

- Include Every Grant: Pell Grants count as income!

- Use a Permanent Address: Use your parents’ home address rather than a dorm; it indicates stability.

- Set Up Autopay: Never, ever miss a payment. One late payment can ruin your score for 7 years.

- Keep Utilization Low: If your limit is $500, don’t spend more than $50 (10%).

- Ask for Increases: Every 6 months, ask the bank to increase your limit (without a “hard pull”).

- Don’t Close Your First Card: The “age of credit” is a huge part of your score.

- Check for “Pre-Approvals” Monthly: Use tools like Experian’s “Credit Match.”

- Use a Co-signer (If Available): Some credit unions still allow co-signers.

- Report Your Rent: Use services like Experian Boost to add your on-time rent and utility payments to your credit report.

- Beware of Annual Fees: Students should never pay an annual fee for their first card.

- Monitor Your Score: Use a free app to track your FICO score monthly.

- Watch Out for “Store Cards”: Avoid Gap or Macy’s cards at first; they have tiny limits and high interest.

- Apply in July/August: Banks often run “Student Specials” right before the fall semester.

- Be Honest: Don’t lie about income. Banks occasionally do “Income Verification” audits.

- Understand APR: If you don’t pay in full, you’ll be charged ~25% interest.

- Avoid Cash Advances: They have immediate interest and high fees.

- Use a Secured Card as a Last Resort: If Discover and Capital One say no, go to OpenSky (no credit check).

- Think Long Term: You are building a 50-year relationship with the financial system.

8. Verified Data: The State of Student Credit in 2026

To understand the risks, look at the latest numbers from the CFPB 2025/2026 College Credit Card Report and Experian’s 2026 State of Credit Cards Report:

- Average Student Balance: ~$3,493 (Source: Experian’s 2026 State of Credit Cards Report).

- Average APR: 22.4% for student cards in early 2026.

- Delinquency Rate: Approximately 9.6% of student credit accounts are 90+ days past due. (Source: Bankrate’s 2026 Credit Card Debt Survey).

- The “Invisible” Population: About 1 in 10 students are “credit invisible,” meaning they have no file at all.

The Danger Zone: High APRs

In 2026, interest rates remain high. According to the CFPB’s 2025 Consumer Credit Card Market Report, consumers were assessed $160 billion in interest charges in 2024, a massive jump from prior years. If you carry a $1,000 balance at 25% APR and only pay the minimum, it will take you over 10 years to pay it off and cost you thousands in interest.

⚠️ The Debt Trap: Interest Paid Over 12 Months

According to CFPB 2025 data on high-interest student accounts, this chart shows the cost of carrying a $1,000 balance at the 2026 average 22.4% APR versus paying in full:

Total Interest Cost (1 Year)

- Paying in Full: $0

- Paying Minimums: ████████████████████ $224+

9. Your “No Income” Questions Answered

Q: Can a student get a credit card with no job?

A: Yes. As long as you have “accessible income” (scholarships, allowances, or savings), you meet the legal requirements for a student card.

Q: Does a student loan count as income?

A: Only the “refund” portion—the money that is paid directly to you for living expenses after tuition is covered—can be listed as income.

Q: Can international students get U.S. credit cards?

A: Absolutely. Look for cards that accept ITINs or passport-based applications like Bank of America or American Express.

Q: What is the easiest student credit card to get?

A: The Discover it® Student or a Secured Credit Card (like the Capital One Platinum Secured) are generally the easiest for beginners.

Q: How much income should I report?

A: Report your “Gross Annual Income.” If you get $500/month from family and a $2,000 summer job, report $8,000.

Q: Will applying hurt my credit score?

A: A formal application (hard pull) will drop your score by 5-10 points temporarily. Always use “Prequalify” tools first to avoid unnecessary drops.

Q: How long does it take to get a 700 credit score?

A: If you get a card today and use it responsibly, you can often hit a 700 score within 6 to 12 months.

Q: What if I am rejected?

A: Wait 30 days, open a checking account at that bank, deposit some cash, and then apply for a Secured Card.

Q: Can I use my partner’s income?

A: If you are 21 or older, you can legally include income from a spouse or partner if you have a “reasonable expectation of access” to it.

Q: Are there cards with no credit check?

A: Yes, cards like OpenSky Secured Visa do not perform a credit check, but they usually require a security deposit.

10. Conclusion: Your Financial Future Starts Now

Getting your first credit card for students USA 2026 is about more than just buying coffee or textbooks. It is about claiming your seat at the table of the U.S. economy.

Remember the story of Alex? After getting a secured credit card for students USA, Alex spent $20 a month on Netflix, paid it off instantly, and six months later had a 710 credit score. When it came time to sign that apartment lease, Alex didn’t need a co-signer. Alex was “credit-ready.”

No income? No problem. Use your scholarships, your family support, and the modern tools of 2026 to build your foundation. Be responsible, stay within your means, and watch your financial resume grow.

–END–

About the Author – Alen Vi

Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer

The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.

Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure

CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.