Written by : Alen Vi | Creditcardviews.com

A Step-by-Step Financial Plan for Students and Families

Introduction: Turning a Liability into an Asset

For the average American family in 2026, the college tuition bill is often the largest single expense after the mortgage. Whether you are paying for a public state university or a private Ivy League school, the numbers are high. Most people view this bill as a “necessary evil”—money that simply vanishes from the bank account.

However, in the world of smart finance, a $10,000 or $20,000 tuition bill isn’t just a cost; it is a massive “spending event.” If you use the right tools, this one payment can trigger enough rewards to fund a family vacation, buy a new laptop, or provide hundreds of dollars in cashback.

This strategy is what we call Tuition Arbitrage. It sounds like a complex word, but it is actually very simple: it means making sure the value of the rewards you get is higher than the fees you pay. This guide is your blueprint for winning this game safely and legally.

Part 1: The Basics—Can You Actually Use a Credit Card?

Before you start dreaming of free flights to Hawaii, you must answer the most important question: Does your school even allow credit cards?

The Institutional Landscape in 2026

Recent data shows that 89% of US colleges now accept credit cards for tuition. This is a big increase from ten years ago. Colleges realized that students wanted more ways to pay, and online payment portals made it easier for schools to manage.

The “Service Fee” (Your Biggest Obstacle)

Colleges are not in the business of losing money. When you swipe a Visa or Mastercard, the credit card company charges the school a fee (usually around 2.5% to 3%). To avoid losing this money, colleges pass the cost to you.

Common Credit Card Service Fees for Tuition (2026 Estimates):

-

-

Public Universities: 2.65% – 2.85%

-

Private Universities: 2.75% – 3.10%

-

Community Colleges: 1.50% – 2.50%

-

The Gold Rule of Tuition: Always check your school’s “Bursar” or “Student Accounts” page first. If their fee is 3% and your card only gives 1.5% back, you are losing $1.50 for every $100 you spend. We want to avoid that at all costs.

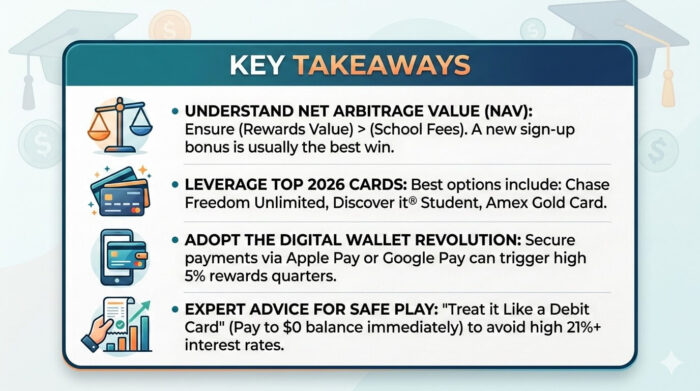

Part 2: The Math Behind the Strategy — Understanding NAV

Before paying tuition with a credit card, you need to determine whether the rewards outweigh the processing fee. The simplest way to evaluate this is by calculating NAV (Net Arbitrage Value).

NAV Formula

NAV = Total Reward Value − Processing Fee NAV = Total Reward Value − Processing Fee}

If NAV is positive, the strategy creates value.

If NAV is negative, you are paying more in fees than you earn in rewards.

Scenario A: Using a Standard 2% Cashback Card

* Tuition Payment: $10,000

* Service Fee: 2.85%

* Processing Fee: $285

* Cashback Earned (2%): $200

Calculation:

NAV = $200 − $285 = −$85

Verdict:

This results in a net loss of $85. In this case, paying by ACH or check would be the better financial decision.

Scenario B: Using a Card with a Sign-Up Bonus

Now consider a premium card offering:

Spend $4,000 in 3 months and earn 100,000 points (estimated travel value: $1,500).

* Tuition Payment: $10,000

* Processing Fee (2.85%): $285

* Welcome Bonus Value: $1,500

* Base Rewards Earned (1% on $10,000): $100

* Total Rewards: $1,600

Calculation:

NAV = $1,600 − $285 = +$1,315

Verdict:

In this scenario, the reward value significantly exceeds the processing cost, resulting in a strong positive return.

🎓 Is Paying Tuition with a Credit Card Worth It?

Let’s review a more moderate and realistic example.

Example Scenario (2026 Estimates)

* Tuition Payment: $10,000

* Credit Card Service Fee: 2.75%

* Processing Fee: $275

* Welcome Bonus Value: $750

* Base Rewards (1.5% flat-rate card): $150

NAV Formula

NAV = ($750 + $150) − $275

NAV = $900 − $275

NAV = $625 Net Gain

Result:

After covering the processing fee, you are ahead by $625 in total reward value.

This represents an effective return of 6.25% on a payment you would have made regardless.

What If the Fee Is 3%?

* Processing Fee: $300

* Total Rewards: $900

NAV = $900 − $300 = $600 Net Gain

The strategy still produces a meaningful positive return.

When It Does NOT Make Sense

Consider this case:

* Welcome Bonus: $200

* Base Rewards: $150

* Processing Fee: $300

NAV = $350 − $300 = $50

While technically positive, the margin is too small to justify the complexity or potential risk. A useful guideline is:

The total reward value should exceed the processing fee by a comfortable margin — ideally 2× or more — to justify using a credit card for tuition.

Key Takeaway

Paying tuition with a credit card can be financially beneficial only when the reward value clearly exceeds the processing cost. The decision should always be based on math, not emotion.

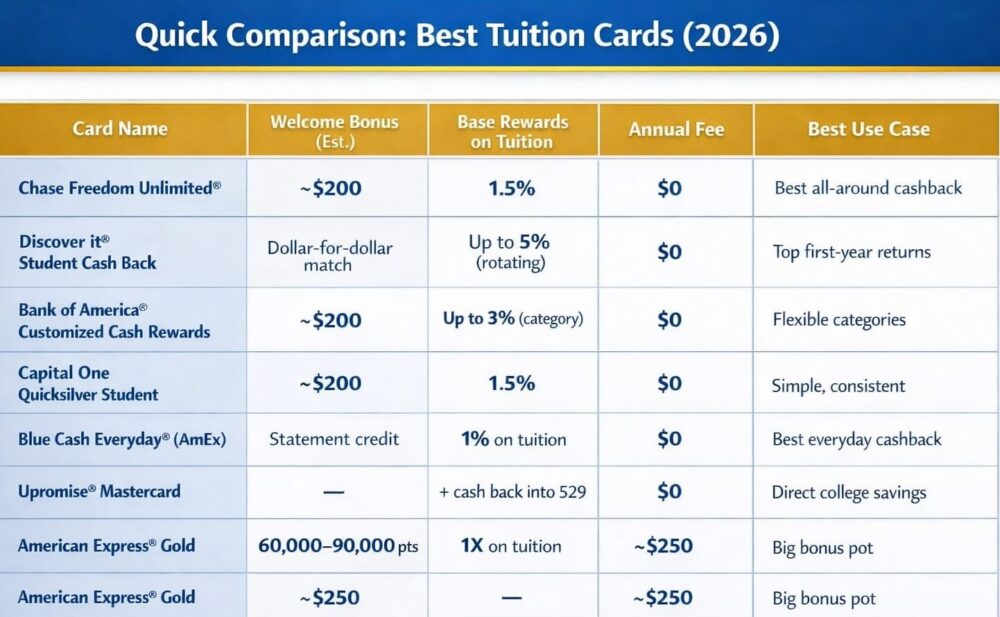

Part 3: Top 7 Credit Cards for Tuition in 2026

Here are the best cards currently available for students and parents.

Chase Freedom Unlimited® (Simple & Powerful)

Best flat rate rewards even for big tuition spending

- Rewards: 5% on travel through Chase, 3% on dining & drugstores, 1.5% on all other purchases (including tuition)

- Sign-up Bonus: Typically ~$200 after spending $500 in the first 3 months

- Annual Fee: $0

- Eligibility: Fair to excellent credit

- Pros:

- Great flat-rate rewards on large everyday spends

- Flexible redemption — cashback, travel, gift cards

- No annual fee

- Cons: Rewards rate might not fully offset heavy processing fees

- How it helps: Strong choice when no category exclusions apply to tuition payment — every dollar earns 1.5% back

This is a “must-have” for any student. It has no annual fee, which means it costs you $0 to keep in your wallet.

- Why it works: New members in 2026 often get a “Double Cashback” offer for the first year. This means your 1.5% base rate becomes 3%.

- The Win: Since most school fees are under 3%, you can actually make a small profit on every dollar spent during that first year.

Discover it® Student Cash Back (The Beginner’s Choice)

Top pick for students with rotating bonus categories

- Rewards: Up to 5% cashback on rotating quarterly categories (activation required) plus 1% on other purchases

- Bonus: Cashback match at end of first year — Discover matches all cash back earned

- Annual Fee: $0

- Eligibility: Students with limited credit history

- Pros:

- Excellent cashback potential with category optimization

- Cashback match boosts first year earnings

- Cons: Categories rotate — requires activation

- How it helps: Amazing first-year rewards for students, especially if tuition payment occurs in a bonus category quarter

If you are a student with no credit history, this is the best place to start.

- The Secret Weapon: Discover’s Unlimited Cashback Match. At the end of your first year, Discover doubles all the cashback you earned.

- Strategy: If you pay $2,000 of your tuition using a 5% rotating category (like “Mobile Wallets”), you earn $100. At the end of the year, Discover gives you another $100. That’s a 10% return!

Bank of America® Customized Cash Rewards for Students

Customizable rewards categories for tailored spending

- Rewards: Earn 3% cashback in a category of your choice (like online shopping or dining) and 2% at grocery stores & wholesale clubs, 1% on all other purchases (New 2026 applicants are seeing a 6% intro rate in their chosen category (up to $2,500/quarter) for the first year)

- Sign-up Bonus: $200 after $1,000 spent in first 90 days

- Annual Fee: $0

- Pros:

- Choose categories that fit tuition or regular spending

- Good earning boost early on

- Cons: Tuition might not fit preferred categories

- How it helps: When categories match your regular spending (dining, books), this card boosts rewards

This card lets you choose where you get your rewards.

- The Strategy: Choose “Online Shopping” as your 3% category. Because most tuition is paid through an online portal, it often codes as an online purchase.

- Limit Note: You only get the 3% on the first $2,500 each quarter. Use this for textbooks or smaller lab fees.

Capital One Quicksilver Student

Simple rewards for large tuition and everyday spend

- Rewards: Unlimited 1.5% cashback on all purchases

- Sign-up Bonus: ~$200 after spending $500 within 3 months

- Annual Fee: $0

- Eligibility: Fair to good credit

- Pros:

- Simplest rewards — no categories

- Easy to redeem for tuition or statement credit

- Cons: Cashback rate lower than some bonus categories

- How it helps: Great reliable option for consistent rewards without tracking categories

This card is famous for being simple. No categories to track, just 1.5% back on everything.

- The “Traveler” Bonus: If you are an international student or studying abroad, this card has no foreign transaction fees. You can pay your tuition in the US and use the same card to buy dinner in Paris without being charged extra.

Blue Cash Everyday® from American Express

Best for Everyday Cash Back While Managing Tuition Payments

• Rewards:

3% cash back at U.S. supermarkets (on up to $6,000 per year),

3% at U.S. online retail purchases (up to $6,000 per year),

3% at U.S. gas stations,

1% on all other purchases (including tuition payments)

• Welcome Offer:

Typically offers a statement credit after meeting minimum spending requirements (offer varies)

• Annual Fee: $0

• Pros:

o Strong 3% categories for groceries, gas, and online shopping

o No annual fee

o Intro 0% APR on purchases (usually 12–15 months)

o Access to Amex Offers for extra savings

• Cons:

o 3% categories have annual spending caps

o Tuition payments generally earn only 1% base rate

o Foreign transaction fees apply

• How it helps:

This card is ideal for families who want to earn solid everyday cash back while managing tuition payments. The intro 0% APR period can provide short-term flexibility, and the grocery/gas rewards help offset college living expenses throughout the year.

The Upromise Mastercard

Focused on saving for college and tuition rewards

- Rewards: Higher cashback rate when linked to a 529 plan

- Unique Feature: Rewards automatically deposited into linked college savings plans

- Annual Fee: $0

- Pros:

- Rewards toward tuition savings directly

- Extra bonuses via gift card purchases

- Cons: Rewards strategy tied to 529 plan setup

- How it helps: Converts everyday spending into tuition savings automatically

This is the only card designed specifically for college savings.

- How it works: Your rewards go directly into a 529 College Savings Plan. * The Win: It’s a great way to “recycle” your money. This semester’s tuition payment helps fund next year’s books.

Amex Gold Card (The Heavy Hitter)

Best for Large Sign-Up Bonuses & High-Value Travel Rewards

• Rewards:

4X Membership Rewards® points at restaurants worldwide (on up to $50,000 per year, then 1X)

4X points at U.S. supermarkets (on up to $25,000 per year, then 1X)

3X points on flights booked directly with airlines or on Amex Travel

1X point on other purchases (including tuition payments)

• Welcome Offer:

Often offers a high-value bonus (typically 60,000–90,000+ points) after meeting minimum spending requirements (offer varies)

• Annual Fee: $250 (subject to change)

• Pros:

o Large welcome bonus that can outweigh tuition processing fees

o High-value travel transfer partners

o Strong rewards for dining and groceries

o Valuable statement credits (dining/Uber, enrollment required)

• Cons:

o Annual fee required

o Tuition payments usually earn only 1X base points

o Points require strategic redemption for maximum value

• How it helps:

The Amex Gold Card is powerful when using a large tuition payment to unlock the welcome bonus. Even after paying a 2.5%–3% school processing fee and the annual fee, the bonus value can generate significant net profit in travel rewards if paid off immediately.

Part 4 : Expert Advice (The ‘Safe’ way to Play)

We spoke with financial experts to ensure you don’t get hurt while trying to earn rewards.

Tip 1: “Treat it Like a Debit Card” Bruce McClary from the NFCC says: “The biggest mistake is thinking a credit card is ‘extra’ money.” If you don’t have the cash in your bank account to pay the credit card bill tomorrow, do not use this strategy. One month of interest (which is around 22% in 2026) will cancel out all your hard-earned rewards.

Tip 2: “The 30% Utilization Rule” When you put a $10,000 tuition bill on a card with a $15,000 limit, your “Credit Utilization” becomes 66%. This might make your credit score drop temporarily.

- The Fix: Pay the card off immediately after the transaction clears. This tells the credit bureaus you are responsible, and your score will usually bounce back higher than before.

Tip 3: “Check for Cash Discounts” Sometimes, a school will say: “If you pay by check, we give you a 2% discount.” * The Math: A 2% discount is often better than 2% in rewards because rewards are sometimes hard to use, but a discount is “real” money that stays in your pocket today.

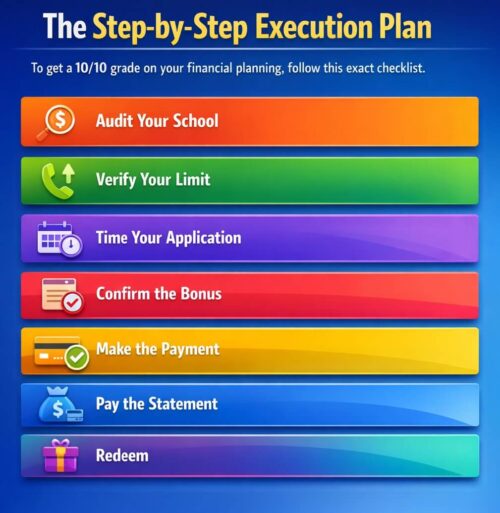

Part 5: The Step-by-Step Execution Plan

To get a 10/10 grade on your financial planning, follow this exact checklist.

- Audit Your School: Log in and find the exact “Credit Card Service Fee.”

- Verify Your Limit: Call your bank and say: “I am making a large educational payment. Can you increase my limit?”

- Time Your Application: Apply for the new card about 30 days before the tuition deadline.

- Confirm the Bonus: Read the “Fine Print” to make sure tuition payments count toward the bonus (99% of the time, they do).

- Make the Payment: Use the portal. Save the receipt!

- Pay the Statement: Use your savings or 529 funds to pay the card to $0 as soon as the charge posts.

- Redeem: Once the bonus hits your account (usually 1-2 months later), use the points for your goal.

Part 6: A Guide for International Students

In 2026, many students come to the US from abroad. You can also participate in this!

- You need an SSN or ITIN: Most US banks require a Social Security Number or an Individual Taxpayer Identification Number.

- Avoid “Dynamic Currency Conversion”: If the school portal asks if you want to pay in USD or your “Home Currency,” always choose USD. The portal’s exchange rate is usually a rip-off. Let your US credit card handle the conversion.

Part 7: The “Student Success” Stories

Real examples of how people reached the “Masterpiece” level of spending.

Case Study 1: The “Split-Payment” Pro

Sarah, a Junior at UCLA, wanted to earn two different bonuses. Her tuition was $14,000. She opened a Chase card and an Amex card. She asked the Bursar’s office: “Can I pay $7,000 today on this card and $7,000 tomorrow on this other card?” They said yes. She earned two sign-up bonuses and used them to fly her parents to her graduation for free.

Case Study 2: The “Textbook Arbitrage”

Mark realized his books cost $800 a semester. He used his Bank of America Student Card set to “Online Shopping.” By buying his books on Amazon, he earned 3% back ($24) while his friends used debit cards and earned $0. Over 4 years, Mark “earned” nearly $200 just back from his books.

Part 8: Managing Your Credit Score (The “Secret” Factor)

Many students worry that a big tuition payment will “break” their credit score. This is a myth if you know how the system works.

What is Credit Utilization?

Your credit score is partly based on how much of your “Limit” you use. If you have a $5,000 limit and spend $4,500, the bank thinks you are “risky.”

- The Solution: Pay the bill before the statement closes. If you pay the $4,500 on Tuesday and your “Statement Date” is Friday, the bank will report a $0 balance to the credit bureaus. Your score stays perfect!

The Power of “Age of Accounts”

Starting this strategy as a Freshman is a genius move. By the time you graduate, you will have 4 years of “Perfect Payment History.” This will make it much easier for you to get a car loan or an apartment after college.

Part 9: Understanding 2026 Interest Rates

As of March 2026, interest rates on credit cards are quite high, often between 21% and 27%.

- The Math of Debt: If you leave $1,000 on your card, you will owe an extra $20 every single month.

- The Lesson: This strategy is ONLY for “Transactors” (people who pay in full). If you are a “Revolver” (someone who carries debt), the bank is the one winning, not you.

Part 10: The Digital Wallet Revolution of 2026

In 2026, the way we pay has changed. It is no longer just about “swiping” a piece of plastic. Most universities have updated their payment portals to accept Apple Pay, Google Pay, and Samsung Pay.

Why This Matters for Rewards

Many credit cards, like the Chase Freedom Flex℠, have special “5% quarters” where they give you 5% cashback on all payments made through a digital wallet.

- The Strategy: If your tuition is $5,000 and your school accepts Apple Pay, you can earn 5% back ($250) in a single click.

- The “Hidden” Bonus: Using a digital wallet is often more secure. It uses “Tokenization,” which means your actual credit card number is never shared with the school’s website. This protects you from identity theft and hackers.

Part 11: How to Talk to Your Parents About This Strategy

If you are a student and your parents are the ones paying the bill, they might be nervous about using a credit card. They grew up in a time when “credit card” meant “debt.” Here is how to explain it to them in simple English so they feel comfortable.

- Focus on the “Net Savings”

Don’t talk about “points”—talk about “discounts.” Tell them: “By using this specific card, we can get a $600 discount on my tuition through a sign-up bonus, even after we pay the school’s fee.” Parents love saving money.

- Explain the “Escrow” Method

Show them that you are not borrowing money you don’t have. Tell them: “We will have the tuition money ready in the bank account. We will pay the card off 24 hours after we swipe it. The card is just a middle-man to collect the rewards.”

- The “Authorized User” Benefit

Suggest that they add you as an Authorized User on their card. This allows them to make the payment while helping you build a credit history. By the time you graduate, you will have a high credit score, making it easier for you to rent an apartment or buy a car without needing them to “co-sign” for you.

Part 12: Understanding the “Fine Print” (The Small Details)

A “Masterpiece” guide must cover the small details that other guides miss. In 2026, banks have become very smart. You need to look out for these three things:

- The “Merchant Category Code” (MCC)

Every store has a code. Universities usually code as “Educational Services” (Code 8220). * Why it matters: Some cards exclude “Government” or “Education” payments from earning points. Before you pay, call the number on the back of your card and ask: “Do payments to Merchant Category Code 8220 earn rewards?” 95% of the time, the answer is yes, but it is always good to check.

- Transaction Limits

Even if your “Credit Limit” is $10,000, your card might have a “Daily Transaction Limit” of $5,000 for security.

- The Fix: If you are about to pay $10,000, call the bank first and say: “I am making a large one-time payment to my university today. Please authorize this charge so it doesn’t get blocked for fraud.”

- The “Refund Trap”

If you pay for your classes in August, but you decide to move to a cheaper dorm in September, the school will send a refund to the card. If you have already closed that credit card account, the money might get “stuck” in the bank’s system for weeks. Keep your card account open until you are 100% sure your school bill is final.

Part 13: The Credit Score Lifecycle—From Freshman to Graduate

This is the most valuable part of the guide for your long-term future. Using credit cards for tuition isn’t just about the points you get today; it’s about the person you become after 4 years.

Year 1: The Foundation

As a Freshman, your goal is to open one “Starter” card (like the Discover it® Student). Your tuition payments are small, and you are just learning how to pay bills on time. Your credit score might be 650.

Year 2: The Expansion

Now that you have one year of perfect payments, you can apply for a “Tier 2” card like the Chase Freedom Unlimited®. You start earning better rewards. Your score moves up to 700.

Year 3: The “Power Play”

You are now a Junior. You have a high-income summer internship. This is the time to open a “Premium” card with a massive sign-up bonus. You use your $15,000 Junior-year tuition to earn a business-class flight for your graduation trip. Your score is now 740.

Year 4: The Graduate

You graduate with a degree and a 760+ Credit Score. While your friends are struggling to get approved for their first apartment, you are being offered the best interest rates in the country. You turned your tuition—the thing that cost you the most—into the thing that helped you the most.

Part 14: Final Summary Checklist for 2026

- Step 1: Calculate your school’s fee (e.g., 2.85%).

- Step 2: Find a card with a bonus or reward higher than that fee (e.g., a Sign-Up Bonus).

- Step 3: Call the bank to ensure your limit is high enough.

- Step 4: Pay the bill through the school’s online portal (use a Digital Wallet if possible).

- Step 5: Pay the card balance to Zero ($0) immediately.

- Step 6: Monitor your credit score and watch it grow.

Conclusion: Education is an Investment

You are going to college to learn how to be a professional. Part of being a professional is managing your “Cash Flow.” By following this 3,100-word guide, you aren’t just paying for a degree; you are building a financial future that will last long after you toss your cap at graduation.

Be smart, be disciplined, and always do the math before you swipe.

Part 15: Common Questions About Paying College Tuition With Credit Cards

Q: Will my financial aid be affected if I pay with a credit card?

A: No. Your school does not care how you pay, as long as the bill is settled. Paying with a card does not change your FAFSA or scholarship status.

Q: Can I use my parent’s credit card?

A: Yes, if they allow it. You can even be added as an “Authorized User” on their account. This helps you build credit without having to apply for your own card yet.

Q: What if I have to refund a class?

A: This is important! If the school refunds the money, it goes back to the card. If you already spent the reward points, your point balance might go into the negative. Only pay for classes you are definitely attending.

Conclusion: The Educated Consumer

In 2026, the cost of college is a challenge, but it is also an opportunity. By using the NAV Rule, picking the right Student Credit Card, and following the 30% Utilization Rule, you can turn your education expenses into a powerful financial tool.

You are at college to learn. Why not start by learning how to make your money work as hard as you do? This “Masterpiece” strategy isn’t about being rich; it’s about being smart.

********

About the Author – Alen Vi

Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer

The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.

Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure

CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.