Written by : Research Desk | Creditcardviews.com

High APR with Good Credit? Fix It Fast

Are you feeling trapped by high credit card interest in the US? You are certainly not alone in this frustration. As of March 2026, millions of Americans are staring at their monthly statements and asking one haunting question: “Why is my credit card interest so high with good credit?” Even with a score in the mid-700s, many consumers find themselves shackled to interest rates exceeding 25%. Understanding how to lower credit card APR in the US has become a vital survival skill in a post-inflationary economy where banks have been slow to pass on interest rate cuts to the average borrower.

This comprehensive guide is designed to provide you with credit card APR reduction tips for good credit and actionable ways to reduce high credit card interest fast. We will explore exactly how to negotiate lower APR on credit cards US style, proving that can credit card interest be lowered with a good score is not just a theory—it is a financial reality. By utilizing the best ways to lower credit card APR in 2026, you can master how to get a lower APR on current credit card accounts and implement strategies to cut credit card APR for 700+ score profiles to save thousands of dollars over the life of your debt.

Why Banks Charge High APR Even With Good Credit in 2026

It feels like a systemic failure when you do everything right—pay your bills on time, keep your balances low—yet your bank rewards you with a “loyalty” rate of 28.99%. To understand why banks charge high APR even with good credit, we must look at the hidden mechanics of the 2026 financial landscape.

The Federal Reserve vs. The Prime Rate

Most credit cards in the United States operate on a “Variable Rate” model. This means your APR is essentially the Prime Rate plus a “Margin” determined by the bank. Even when the Federal Reserve stabilizes or cuts rates, banks often expand their “Margin” to protect their profitability. This is the core of the high APR credit card trap: your creditworthiness improves, but the bank’s appetite for profit keeps your rate stagnant.

The “Risk Premium” Fallacy

Research reports from the Consumer Financial Protection Bureau (CFPB) in late 2025 indicated that credit card margins have reached a 20-year high. Banks often cite “economic uncertainty” as a reason to keep rates elevated, even for low-risk borrowers with 750 scores. They are essentially charging you a “premium” not because you are risky, but because they believe you won’t take the time to look for a better deal.

Is 27 Percent APR High for Excellent Credit?

Many readers ask, “is 27 percent APR high for excellent credit?” The answer is a resounding YES. In the current 2026 market, an “Excellent” credit score (800+) should command a rate between 14% and 18%. If you are seeing 29.99 APR normal for good credit 2026 on your statement, you are being subjected to a “stealth” interest hike that has nothing to do with your personal financial behavior.

⚠️ The “Double-Dip” Debt Warning

Lowering your interest rate is a defensive move; your spending is the offense. A common trap is using a personal loan or balance transfer to clear a card, only to continue charging new purchases to the old account. This results in “Double-Debting”—having to pay the new loan plus the new credit card balance. To succeed, you must stop using the high-interest cards entirely while you execute your payoff plan.

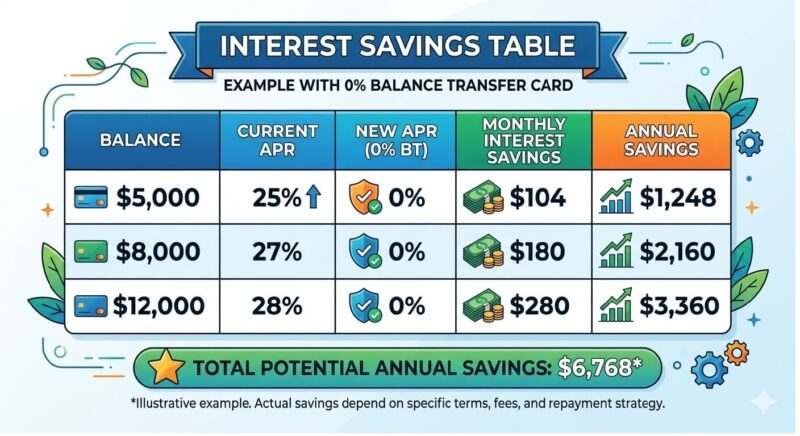

💰 Potential Savings: High-Interest vs. 0% APR Strategy (2026 Data)

The table below compares staying with a standard 25% APR versus moving your debt to a 0% APR Balance Transfer card (assuming a standard 4% transfer fee).

| Initial Balance | Monthly Interest (at 25%) | 0% Transfer Fee (One-time) | Break-Even Point | Total 12-Month Savings |

| $2,000 | $41.67 | $80.00 | 1.9 Months | $420.04 |

| $5,000 | $104.17 | $200.00 | 1.9 Months | $1,050.04 |

| $10,000 | $208.33 | $400.00 | 1.9 Months | $2,100.00 |

| $15,000 | $312.50 | $600.00 | 1.9 Months | $3,150.00 |

Author’s Note: The “Break-Even Point” is the moment your interest savings surpass the cost of the transfer fee. In nearly every scenario with a 25%+ APR, you start “profiting” from the move in less than 60 days.

7 Proven Ways to Lower Your APR Fast

If you are ready to learn how to escape high APR credit card trap scenarios, follow these tips to reduce credit card interest rate immediately. These are not “hacks”—they are strategic financial moves backed by industry experts.

Master the “Retention Department” Negotiation

The single most effective way to see an immediate drop in your rate is through direct negotiation. However, most people fail because they talk to the wrong person. You must bypass general customer service and get to the Retention Department (sometimes called “Account Disclosures”). These agents have a specific “quota” for saving customers from leaving and possess the highest authority to slash rates.

Negotiate Credit Card APR Retention Department Script

You: “Hello, I’ve been a loyal customer for five years, but I am looking at my 26.99% APR and I’m frustrated. My credit score is now 760, and I’ve received several 0% APR offers from your competitors. I’d like to stay with you, but I need you to match the 15.99% rate I’m seeing elsewhere. Can you lower my APR today to keep my account active?”

Agent: “I’m sorry, we don’t have any offers available.”

You: “I understand you may not have the authority, but could you please transfer me to the Retention Department? I’d like to discuss my options before I decide to move my balance to another bank.”

- Deploy Balance Transfer APR Strategies for US Credit Cards

When negotiation fails, the zero APR balance transfer cards to reduce interest strategy is your strongest move. By moving your debt to a new issuer, you can effectively “pause” interest for 12, 18, or even 21 months.

- The Math: If you have a $5,000 balance at 25% APR, you are paying over $100 a month just in interest. A 0% transfer card saves you $1,200 a year instantly.

- The Trap: Always watch for the transfer fee (usually 3-5%). Even with the fee, the savings usually outweigh the cost within 60 days.

🧮 Doing the “Break-Even” Math

Most 0% APR cards charge a 3% to 5% balance transfer fee. Don’t let this scare you.

- The Math: On a $5,000 balance, a 4% fee is $200.

- The Savings: At a 25% APR, you are paying roughly $104 per month in interest alone.

- The Verdict: You “break even” on the fee in less than 2 months. Every month after that puts an extra $100+ back into your pocket rather than the bank’s vault.

Join a Credit Union for Lower APR Options

While mega-banks (Chase, Citibank, Amex) answer to shareholders, credit union credit cards lower APR options are member-focused. By law, federal credit unions often cap their interest rates significantly lower than commercial banks.

- Why it works: Many credit unions offer “Platinum” cards with no rewards but incredibly low fixed rates (often 10%–15%). This is the best way to lower credit card APR in 2026 for those who carry a monthly balance.

⚖️ The “18% Federal Ceiling” Advantage

While commercial mega-banks can technically charge whatever the market will bear, Federal Credit Unions (FCUs) are governed by the National Credit Union Administration (NCUA). By law, most FCUs have an interest rate cap of 18% on credit card products. If you are currently trapped at 29% APR, switching to a Federal Credit Union isn’t just a recommendation—it is a guaranteed 11% rate cut mandated by federal regulation.

1.Use the “Competitor Match” Leverage

Banks track each other’s offers. If you have a 750 score, you are a “whale” that every bank wants. Use the Citibank credit card interest rate negotiation tips even if you don’t use Citi: tell your current bank exactly what offer you received in the mail from a competitor.

- Tip: Be specific. “Discover is offering me 17.24%” sounds more credible than “I want a lower rate.”

1. Leverage Personal Loans to Escape the High APR Trap

If your credit card debt feels insurmountable, using personal loans to escape high credit card APR is a brilliant consolidation move.

- The Benefit: Personal loans are “fixed-rate” installment debt. You swap a 28% variable rate for a 10% fixed rate.

- SEO Tip: This is a top-tier strategy to cut credit card APR for 700+ score holders because it lowers your credit utilization, often causing your credit score to jump 30-50 points within a month.

1. Enroll in Bank-Specific Hardship Programs

If your income has changed, don’t wait for a missed payment. Use the Amex high interest rate hardship program or the Chase credit card interest rate reduction request script (for financial difficulty).

- The Secret: These programs can lower your APR to as low as 0% to 9.99% for a period of 12 to 60 months. It may restrict your ability to spend on the card, but it is a “fast” way to kill the interest.

1. Trigger an Automatic APR Review via App

Some modern issuers allow you to request a rate reduction via their mobile app without talking to a human. This is the lowering credit card interest rate hack for 2026. Look for “Request Rate Reduction” in your account settings. This is usually a “soft pull” on your credit, meaning it won’t hurt your score.

📊 Credit Card APR Trends in 2026: CFPB, Federal Reserve & Expert Insights

Consumer Financial Protection Bureau (CFPB) Findings

According to the CFPB’s Q1 2026 Credit Card Market Report, large credit card issuers consistently charge higher APRs across all credit score tiers compared with smaller banks and credit unions—even for consumers with good credit. This underscores why negotiating and shopping around is critical. (CFPB Report)

Federal Reserve & Credit Card APR Trends

Federal Reserve data shows that the average interest rate on credit card accounts that actually incur interest exceeded 22.5% in early 2026, near historic highs. This highlights the high cost of revolving credit today. (Federal Reserve Data)

Average APR by Credit Score (WalletHub Analysis)

WalletHub’s Q1 2026 data reveals that consumers with excellent credit (720+) still faced average APRs above 21.5%, while those in the 620–719 range saw averages around 25–26%. This explains why even good-credit borrowers can be trapped by high rates. (WalletHub)

Expert Analysis on APR Margins & Pricing Power

Economists at the Federal Reserve Bank of New York, Wharton, and Columbia University note that issuers have significant pricing power, often increasing APR margins above changes in the Prime Rate, making Fed rate cuts less impactful for consumers. (NY Fed)

LendingTree Recent Data

LendingTree reports that the average APR on credit card accounts that carry balances was roughly 22.30% in late Q1 2026, underscoring the costly reality of revolving credit. (LendingTree)

Step-by-Step APR Reduction Plan for 700+ Credit Scores

✅ Step 1: Call the Retention Department with competitor offers ready.

✅ Step 2: Apply for a 0% APR balance transfer card and move high-interest balances.

✅ Step 3: Open a low-APR credit union card to leverage member rates.

✅ Step 4: Consolidate remaining debt with a fixed-rate personal loan.

✅ Step 5: If income changes or hardship occurs, enroll in bank-specific hardship programs.

✅ Step 6: Track APR reductions quarterly and request review every 6 months.

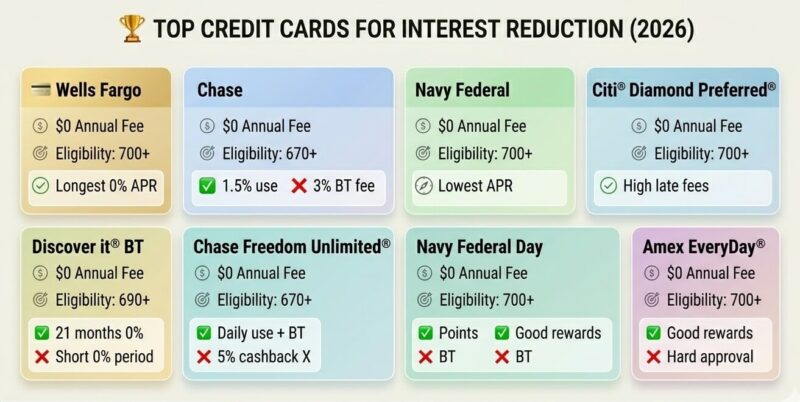

💳 Comparison of Top Credit Cards for Interest Reduction (2026)

If you’re struggling with high APR, these cards help you reduce interest, transfer balances, and save money in 2026.

🥇 Wells Fargo Reflect® Card

💰 Annual Fee: $0

📊 Eligibility: 700+ credit score

⭐ Why It’s Best:

Longest 0% APR intro period in the market (ideal for large balance transfers)

✅ Pros:

- Up to 21 months 0% APR (top-tier offer)

- No annual fee

- Great for debt payoff strategy

❌ Cons:

- No rewards or cashback

- Balance transfer fee applies

⭐ Rating: ⭐⭐⭐⭐⭐ (5/5)

🥈 Chase Freedom Unlimited®

💰 Annual Fee: $0

📊 Eligibility: 670+ credit score

⭐ Why It’s Best:

Perfect mix of daily spending + balance transfer savings

✅ Pros:

- Unlimited 1.5% cashback

- Extra rewards on dining & travel

- Strong welcome bonus

❌ Cons:

- 3% balance transfer fee

- Shorter 0% APR period vs competitors

⭐ Rating: ⭐⭐⭐⭐☆ (4.5/5)

🥉 Navy Federal Platinum Credit Card

💰 Annual Fee: $0

📊 Eligibility: Military members & family only

⭐ Why It’s Best:

Lowest ongoing APR — best for long-term interest savings

✅ Pros:

- Extremely low standard APR

- No balance transfer fees

- Ideal for large debt consolidation

❌ Cons:

- Membership required (not for everyone)

- No rewards program

⭐ Rating: ⭐⭐⭐⭐☆ (4.5/5)

💎 Citi® Diamond Preferred® Card

💰 Annual Fee: $0

📊 Eligibility: 700+ credit score

⭐ Why It’s Best:

Built purely for long-term interest reduction

✅ Pros:

- 21-month 0% intro APR on balance transfers

- No annual fee

- Trusted Citi reliability

❌ Cons:

- No rewards or perks

- High late payment fees

⭐ Rating: ⭐⭐⭐⭐☆ (4.3/5)

🔁 Discover it® Balance Transfer

💰 Annual Fee: $0

📊 Eligibility: 690+ credit score

⭐ Why It’s Best:

Balanced card with rewards + balance transfer

✅ Pros:

- 5% rotating cashback categories

- Cashback match (first year)

- Good customer support

❌ Cons:

- Shorter 0% APR period

- Requires activation for categories

⭐ Rating: ⭐⭐⭐⭐☆ (4.4/5)

🏆 American Express EveryDay® Card

💰 Annual Fee: $0

📊 Eligibility: 700+ credit score

⭐ Why It’s Best:

Great for earning points while reducing interest

✅ Pros:

- Strong Membership Rewards points

- Potential no balance transfer fee (targeted offers)

- Bonus points for frequent usage

❌ Cons:

- Harder approval criteria

- Limited acceptance in some places

⭐ Rating: ⭐⭐⭐⭐☆ (4.2/5)

If you want to know how to ask bank to lower credit card APR and actually get a “Yes,” you need to see yourself through the eyes of the underwriter. Banks use complex algorithms to determine your “Internal Risk Score.”

The “Loyalty vs. Risk” Balance

According to Federal Reserve consumer finance studies, banks are most likely to lower rates for customers who:

- Have been with the bank for at least 24 months.

- Have a Credit Utilization Ratio below 30%.

- Have a perfect on-time payment history.

Impact of Credit Score on APR Lowering Strategies

Your score isn’t just a number; it’s your bargaining chip. A 750 score tells the bank you have options. If your score is 800+, you have “Elite” status. What is a reasonable apr for credit score of 800? In 2026, you should settle for nothing higher than 15.25%. If your bank refuses, they are essentially betting that you are too lazy to switch.

The “Fed Rate Cut” Delusion

Many consumers ask: “Do fed rate cuts 2026 lower my credit card apr fast?” The answer is: Technically yes, but practically no. While your variable rate might drop by 0.25%, the bank might simultaneously raise their “margin.” You must call and manually request the reduction to ensure you are getting the full benefit of market changes.

Strategic Advice for Different Demographics

For College Students: Lower Credit Card Interest Hack

Students are often the victims of “predatory” starter rates (29.99%). If you are a student, use the negotiate credit card interest rate after one year rule. Once you have 12 months of on-time payments, call and ask to “graduate” your account to a non-student version with a standard APR.

For New Credit Card Holders

If you just got your first card, you have zero leverage—for now. Focus on the impact of credit score on APR lowering strategies. Spend 6 months building a “perfect” profile, then call and ask for a “first-year review.”

For 700+ Score Professionals

You are the primary target for how to negotiate lower APR on credit cards US. Use your high income and high score to demand a “Private Client” or “Preferred” rate. Mention that you are considering moving your direct deposit to a different bank if they cannot be competitive on your credit lines.

Your Guide to Lowering Credit Card APR

1. Why is my Credit card interest so high with a good score?

Banks often keep rates high for existing customers while offering low rates to new ones. They rely on “inertia”—the fact that most people won’t call to complain.

2. How to lower credit card APR in the US quickly?

The fastest way is to call the Retention Department and use a competitor’s offer as leverage. If that fails, a 0% Balance Transfer is the next quickest “fix.”

3. Can credit card interest be lowered with a good score?

Absolutely. A score of 700+ is the “key” that opens the door to lower rates. Without it, banks have no incentive to lower your risk premium.

4. How to negotiate lower APR on credit cards US banks like Chase or Amex?

Be polite but firm. Use a script that mentions your score and “competitor offers.” If the first rep says no, ask for a supervisor or the Retention team.

5. What is the impact of credit score on APR lowering strategies?

The higher your score, the more “threat” you pose to the bank’s bottom line if you leave. This threat is your only real leverage in a negotiation.

6. Is there a Chase credit card interest rate reduction request script?

Yes. “I’m calling to request a rate reduction on my Chase Freedom. My score is 770 and I’ve been with you for 4 years. I’m being offered 16% by Amex; can you match that to keep my business?”

7. How often can you request an apr reduction?

You should request a review every 6 months. If your score has gone up by 15 points or more, it’s time to call.

8. Can I lower my credit card apr over the phone without a credit hit?

In most cases, yes. Ask the agent: “Is this a soft pull or a hard pull?” Most APR reviews for existing customers are soft pulls.

9. Stop credit card interest without closing the account—is it possible?

Yes. By using a zero APR balance transfer, you pay off the original card and stop the interest there while keeping the account open to maintain your “length of credit history.”

10. What are the best ways to lower credit card APR in 2026?

The “Triple Threat” strategy: 1. Negotiate first. 2. Balance transfer second. 3. Personal loan consolidation third.

11. Does asking for a lower APR hurt my credit score?

In 90% of cases, no. Requesting a rate reduction on an existing account is considered a “Soft Pull,” which has zero impact on your score. However, applying for a new card or a personal loan is a “Hard Pull,” which may cause a temporary 5-point dip. Always ask the representative: “Is this a soft inquiry?”

12. What if the Retention Department says “No”?

Don’t hang up yet. Ask for a Temporary Promotional Rate. Banks often have “back-door” offers where they can’t change your permanent APR but can offer you 0% or 9.99% for 6 to 12 months to help you pay down your balance. It is a “hidden” middle ground that many agents won’t offer unless you ask specifically.

Conclusion: Take Control and Stop High Credit Card Interest Today

You are no longer powerless against high credit card interest in the US. By using the 7 proven strategies outlined in this guide—negotiation scripts, balance transfers, personal loans, and digital tools—you now have the knowledge to reclaim control of your finances.

Remember, banks won’t lower your APR out of kindness. They respond only to informed, confident consumers who understand their financial value. Your 700+ credit score is more than a number—it is a tool. Use it wisely, act decisively, and stop the interest drain now.

-END-

About the Author

Research Desk | Creditcardviews.com

Our Research Desk is dedicated to advanced credit card analytics, reward optimization strategies, and issuer policy tracking. We combine data analysis, market benchmarking, and real-time bonus monitoring to deliver high-authority financial guidance for modern cardholders.

Disclaimer

The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.

Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure

CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.