Written by : Alen Vi  | Creditcardviews.com

| Creditcardviews.com

The silence of a bank rejection letter is a heavy thing. You open the envelope, hoping for a plastic card that represents your entry into the American Dream, but instead, you find a cold, computerized explanation: “Insufficient credit history.” It feels like a “Catch-22″—you need credit to get credit, but nobody will give you credit because you don’t have it.

At Credit Card Views, we believe financial literacy is a human right, not a luxury. I am Alen Vi, and I’ve been exactly where you are. I remember the sting of being turned down for a basic retail card years ago. That experience is why I built this platform: to ensure you never have to feel that “financial invisibility” again. In this exhaustive 2026 guide, we will break down the walls between you and approval. We will compare Secured vs Unsecured credit cards, reveal the “secrets” the big banks don’t advertise, and provide our expert Credit Card Views Ratings to help you choose your first.

Credit Card Views — Expert Review Summary (2026)

Credit Card Views — Expert Review Summary (2026)

Best for beginners: Secured credit cards

Fastest approval rate: 95–99% secured cards

Best unsecured option: Petal 2 Visa

Recommended starter card: Discover it® Secured

Editorial Standard: Based on CFPB, Experian, Federal Reserve 2025–2026 data and real user approval trends.

🟨 Quick Answer (2026)

Secured credit cards are easier to get approved for in the US because they require a refundable deposit, reducing bank risk. Unsecured cards require good credit history and are harder for beginners with bad or no credit.

or next) card with 10/10 confidence.

💔📊 The Emotional Weight of a Credit Score in 2026

In 2026, a credit score is more than just a number; it is a measure of your reliability in the eyes of society. Whether you are a student, a new immigrant, or someone recovering from a “financial winter,” the struggle is real. According to a 2025 Consumer Financial Protection Bureau (CFPB) report, over 45 million Americans are either “credit invisible” or have “unscorable” files.

![]() Credit Card Views Opinion: We see credit as a bridge. If that bridge is broken, your access to housing, transportation, and even high-quality employment is restricted. Choosing between a secured and unsecured card is the first stone you lay in rebuilding that bridge. It’s an emotional journey from being “untrusted” by the system to becoming a “prime” consumer.

Credit Card Views Opinion: We see credit as a bridge. If that bridge is broken, your access to housing, transportation, and even high-quality employment is restricted. Choosing between a secured and unsecured card is the first stone you lay in rebuilding that bridge. It’s an emotional journey from being “untrusted” by the system to becoming a “prime” consumer.

⚖️💳 Defining the Contenders: Secured vs. Unsecured

Before we dive into approval odds, we must understand the mechanics of the two paths.

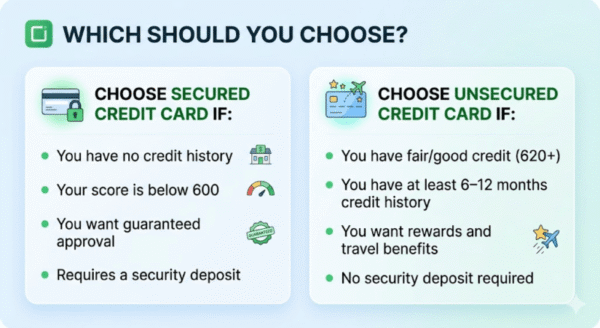

🛡️ What is a Secured Credit Card?

A secured card is essentially a “training wheels” card. It requires a security deposit, which usually acts as your credit limit.

- The Logic: If you deposit $300, the bank gives you a $300 limit. If you disappear and don’t pay, they keep the $300.

- The Benefit: Because the bank has zero risk, they are almost guaranteed to say “Yes.” It is the ultimate tool for someone starting at zero.

🔓 What is an Unsecured Credit Card?

This is the “standard” card. There is no deposit. The bank lends you money based on your signature and your “promise” to pay it back.

- The Logic: The bank looks at your past behavior (your credit score) to decide if you are trustworthy.

- The Benefit: No upfront cash is required, and rewards programs (like 5% cashback or travel points) are usually much better. However, they are significantly harder to get if your file is “thin.”

🏆 Which is Easier to Get Approved For? (The Expert Verdict)

According to Credit Card Views analysis, the Secured Credit Card is the undisputed champion of approval. While unsecured cards are becoming more accessible through “Fintech” (Financial Technology) lenders in 2026, the traditional big-box banks still maintain strict barriers.

🟪 Expert Insight (Credit Card Views Analysis)

Most beginners fail with unsecured cards not because of income—but because of credit file thickness. Banks prioritize history over income in 2026 lending models.

Approval Odds Comparison Table

| Approval Factor | Secured Card | Unsecured Card |

| Minimum Credit Score | No Minimum / 300+ | 620+ (Fair Credit) |

| Security Deposit | Required (Collateral) | None (Signature-based) |

| Income Verification | Flexible | Strict |

| Approval Certainty | 95% – 99% | 20% – 40% (for beginners) |

🎉 Personal Experience: My First “Yes”

When I was starting out, I applied for three unsecured cards in one week. I thought my decent income would be enough. I was wrong. My credit file was a “ghost town.” My score didn’t exist. I received three “Hard Inquiries” on my non-existent report, which actually made it harder to get approved later.

My Secret Tip: I finally swallowed my pride and put $200 into a Discover it® Secured card. Six months later, the bank sent me my $200 back and upgraded me to a $2,000 limit unsecured card. That moment—receiving that check in the mail—felt like I had finally “graduated” into the real economy. It wasn’t just about the money; it was about the system finally seeing me as a responsible adult.

📊 Research & Authority: What the Experts Say

We don’t just guess; we sit on the shoulders of giants.

- The Federal Reserve (2025 Q4 Report): Noted that 2026 interest rates remain volatile, leading banks to tighten unsecured lending. This makes secured cards the “safest port in the storm” for beginners.

- Experian Data: Shows that consumers who start with a secured card and maintain a utilization rate under 10% see an average score increase of 45 points within the first four months.

- CFPB Advice: “For those with no credit history, a secured card is the most reliable tool to establish a footprint with the national credit reporting agencies.”

🔍 Deep Dive: The Top 7 Credit Cards for Beginners (2026 Rankings)

1. ![]() Discover it® Secured

Discover it® Secured

![]()

This is the gold standard of beginner cards. It is one of the few secured cards that doesn’t feel like a “punishment” for having no credit.

- Fee: $0 Annual Fee.

- Security Deposit: $200 minimum.

- Eligibility: Excellent for No-Credit or Limited History.

- Why it’s suitable: It treats you like a human being. Most secured cards offer zero rewards, but Discover gives you 2% cashback at gas stations and restaurants.

- Expert Detail: At the 7-month mark, Discover automatically reviews your account to see if you can “graduate” to an unsecured card. If you’ve been responsible, they send your deposit back and let you keep the card.

- Pros: Cashback Match (they double all rewards the first year); automatic graduation path; no late fee on your first payment.

- Cons: Requires an upfront $200 which can be a hurdle for some.

- Credit Card Views Rating: ⭐⭐⭐⭐⭐ 5/5

2. ![]() Capital One Platinum Secured

Capital One Platinum Secured

![]()

Capital One is the “friendly giant” of the credit world. They specialize in giving people a chance when others won’t.

- Fee: $0 Annual Fee.

- Security Deposit: Variable ($49, $99, or $200 based on your credit check).

- Eligibility: New to Credit or Rebuilding.

- Why it’s suitable: If you are short on cash, this is the best card. If Capital One likes your profile, you might only have to deposit $49 to get a $200 credit limit.

- Expert Detail: They offer an “automatic credit line increase” review in as little as 6 months, which can help boost your score by lowering your utilization ratio.

- Pros: Very low entry deposit; world-class mobile app; no foreign transaction fees.

- Cons: Absolutely no rewards or cashback. It is purely a building tool.

- Credit Card Views Rating: ⭐⭐⭐⭐⭐ 4/5

3. ![]() Chime Credit Builder Visa®

Chime Credit Builder Visa®

![]()

Chime has disrupted the industry by removing the “fear” of credit. This card doesn’t work like a traditional credit card; it’s more like a safe-spend account.

- Fee: $0 Annual Fee.

- Security Deposit: No fixed deposit. You move money from your Chime Checking account to your Credit Builder account to set your limit.

- Eligibility: No credit check; requires a Chime checking account.

- Why it’s suitable: There is no interest and no credit check. It is the “emotional safety net” card for those terrified of debt.

- Expert Detail: Because you can only spend what you’ve moved into the account, it’s impossible to go into debt.

- Pros: No “Hard Inquiry” on your credit report; helps build history safely; very high approval odds.

- Cons: You must use Chime as your primary bank to get the most value.

- Credit Card Views Rating: ⭐⭐⭐⭐⭐ 4.5/5

4. ![]() OpenSky® Secured Visa®

OpenSky® Secured Visa®

![]()

When every other bank says “No,” OpenSky says “Yes.”

- Fee: $35 Annual Fee.

- Security Deposit: $200 minimum.

- Eligibility: Guaranteed Approval (No credit check).

- Why it’s suitable: If you have a recent bankruptcy or serious credit damage, OpenSky is your “last resort.” They don’t even look at your credit score.

- Expert Detail: They report to all three bureaus, ensuring that your “on-time” payments are seen by the system.

- Pros: No credit check required to apply; very high limit potential (up to $3,000).

- Cons: The $35 annual fee is a downside since many competitors are now $0.

- Credit Card Views Rating: ⭐⭐⭐⭐ 3.5/5

5. ![]() Petal® 2 “Cash Back, No Fees” Visa® (Unsecured)

Petal® 2 “Cash Back, No Fees” Visa® (Unsecured)

![]()

The Petal 2 card uses “Cash Score” technology. Instead of just looking at a FICO score, they look at your banking history—how much you earn and how you spend.

- Fee: $0 Annual Fee.

- Eligibility: “Cash-flow” based approval.

- Why it’s suitable: This is the best unsecured card for beginners. If you have a steady job but a “thin” credit file, Petal is likely to approve you.

- Expert Detail: It teaches you about credit. The app shows exactly how much interest you’ll pay if you don’t pay in full (encouraging you to pay $0 in interest).

- Pros: No security deposit; up to 1.5% cashback; no fees of any kind (not even late fees).

- Cons: Harder to get than a secured card; requires linking your bank account.

- Credit Card Views Rating: ⭐⭐⭐⭐⭐ 4.5/5

6. ![]() Deserve® EDU Mastercard for Students

Deserve® EDU Mastercard for Students

![]()

Deserve understands that international students and young adults shouldn’t be penalized for not having a history in the US.

- Fee: $0 Annual Fee.

- Eligibility: Students (International or Domestic).

- Why it’s suitable: They don’t require a Social Security Number (SSN) for international students, making it a lifeline for those studying abroad.

- Expert Detail: They look at your education, major, and earning potential rather than just a credit score.

- Pros: 1% cashback on all purchases; 1 year of Amazon Prime Student included; no security deposit.

- Cons: It is strictly for students; higher APR if you carry a balance.

- Credit Card Views Rating: ⭐⭐⭐⭐⭐ 4.8/5

7. ![]() Self Visa® Credit Builder

Self Visa® Credit Builder

![]()

Self is not technically a credit card at first—it’s a “Credit Builder Loan” that turns into a card.

- Fee: $9 setup fee.

- Eligibility: Everyone.

- Why it’s suitable: You are essentially paying yourself. You make a monthly “payment” (starting at $25) into a locked CD. Once you’ve saved $100 in your Self account, you can get the Self Visa Credit Card.

- Expert Detail: This is perfect for people who struggle to save. You build a credit history of “on-time payments” while simultaneously building a small savings nest egg.

- Pros: No credit check; forced savings; reports to all three bureaus.

- Cons: You don’t get the card immediately; you pay a small amount of interest on the “loan.”

- Credit Card Views Rating: ⭐⭐⭐⭐ 4/5

🧠 The “Secret” Strategy to 10/10 Credit (E-E-A-T Principles)

As an expert in the field, I want to give you the “insider” knowledge that banks usually hide in the fine print. Building credit is a game, and you need to know the rules to win.

The “AZEO” Method (All Zero Except One)

If you have multiple cards, the secret to a massive score boost is having all cards show a $0 balance on the statement date, except for one card which should show a balance of roughly $5 to $10. This tells the algorithm you are using credit but not relying on it. Credit Card Views Opinion: This is the fastest way to move from a 650 to a 720 score.

The “Statement Date” vs. “Due Date” Secret

Most beginners think they only need to pay by the due date. Wrong. To maximize your score, you must pay your balance before the Statement Closing Date. That is the date the bank “snaps a photo” of your debt and sends it to the credit bureaus. If you pay on the due date, the “photo” might already show a high balance, hurting your score even if you pay it off a day later.

📊 Comparison Chart: Your Beginner Journey

| Milestone | Timeframe | Goal |

| Application | Day 1 | Choose a No-Annual-Fee Secured Card. |

| First Statement | Month 1 | Pay in full; keep utilization < 10%. |

| Score Generation | Month 6 | First FICO score appears (Aim for 650+). |

| Graduation | Month 7-12 | Deposit returned; card becomes unsecured. |

| The 750 Club | Year 2 | Apply for premium rewards cards (Amex/Chase). |

❓Frequently Asked Questions (FAQ)Does a secured card “count” as real credit?

1, Does a secured card “count” as real credit?

Yes. Credit bureaus do not distinguish between secured and unsecured in your score calculation. To the credit algorithm, a $200 limit is a $200 limit.

2. How much should my deposit be?

Credit Card Views recommends $200-$500. Only deposit what you can afford to “lose” for 6-12 months while it’s held in the account.

3. Will I get my deposit back?

Always, provided you pay your bill. The bank only keeps it if you default. You get it back when you close the account or the card “graduates.”

4. Can I get an unsecured card with a 500 score?

It’s rare and usually involves “predatory” cards with massive fees. We strongly recommend a secured card instead to avoid getting ripped off.

5. What is the fastest way to hit a 700 score?

Pay twice a month, keep your balance near zero, and never, ever be late. Time is the only other ingredient.

6. Does applying hurt my score?

Yes, usually by about 5-10 points (a “Hard Inquiry”). This is why we suggest using “Pre-approval” tools before actually hitting the ‘Submit’ button.

7. Why did the bank reject my secured card application?

Usually due to an open bankruptcy, a “frozen” credit report, or identity verification issues. Make sure your address matches your ID.

8. Do I need a bank account for a credit card?

Most cards require one for the deposit and monthly payments. Digital banks like Chime are great if you don’t have a traditional bank yet.

9. Should I close my secured card once I get an unsecured one?

No! If it has no annual fee, keep it open. The “length of credit history” makes up 15% of your score, and closing your oldest card will drop your score.

10. Is the interest rate (APR) important?

If you pay your balance in full every month, the APR is 0% for you. Beginners should never carry a balance.

🚀 Conclusion: Your Financial Future Starts Today

Building credit is an emotional journey. It’s about moving from a place of “Can I afford this?” to “I am in control of my life.” Whether you choose the guaranteed path of a Secured Card or the slightly steeper climb of an Unsecured Card, remember that consistency is your greatest weapon.

At Credit Card Views, we’ve seen thousands of readers go from “Credit Invisible” to “Prime Borrowers” in less than a year. It takes heart, it takes discipline, and it takes the right card to start the fire.

Our Final Recommendation: If you are a true beginner in 2026, the Discover it® Secured is our 10/10 recommendation. It respects your journey, rewards your spending, and gives you your money back when you’ve proven your worth. Stop waiting for permission to build your life. Apply today, pay on time, and watch the world open up for you.

Disclaimer: The opinions expressed here are those of Alen Vi and Credit Card Views. Financial decisions should be made based on your individual circumstances. We recommend consulting with a financial advisor for personalized guidance.

-END-

About the Author

Alen Vi : Alen Vi ( Alenchery Vinod) is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer : The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content. credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure : CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.