Written by : Alen Vi | Creditcardviews.com

The journey of an international student is defined by courage and ambition. You have likely spent months, if not years, preparing for this transition—securing admissions, navigating visa interviews, and coordinating a move across the globe. However, many students encounter a significant, often invisible hurdle upon arrival: the American credit system.

In the U.S. financial landscape, your credit score often dictates your access to essential services. Without an established history, simple tasks like renting an apartment, securing a fair interest rate on a car loan, or even signing up for a post-paid cellular plan can become unnecessarily complicated and expensive. This guide is designed to provide a realistic, professional, and actionable 30-day roadmap to help you establish a reliable credit foundation without the hype or overstatements.

Phase 1: The Documentation Foundation (Days 1–7)

The first week of your journey is dedicated to administrative clarity. Before you can build credit, you must be “visible” to the financial system.

Navigating the SSN and ITIN Requirements

A common misconception is that you cannot build credit without a Social Security Number (SSN). While an SSN is a primary identifier, it is not the only path.

- The SSN Path: If you have secured on-campus employment, you are generally eligible for an SSN. You should coordinate with your university’s International Student Services (ISS) office to begin this process as soon as possible.

- The ITIN Alternative: If you are not eligible for an SSN, you can often apply for an Individual Taxpayer Identification Number (ITIN). Many major lenders now accept ITINs for credit applications, which allows you to start building history even without an active job.

- Expert Insight: According to general guidelines from the Consumer Financial Protection Bureau (CFPB), lenders use these identification numbers to accurately report your payment habits to the three major credit bureaus: Experian, TransUnion, and Equifax.

Strategic Banking Choices

Your choice of a primary bank can influence your future credit approvals. In many cases, it is beneficial to open a checking account at a bank that also offers student credit products.

- The “Relationship” Factor: Having a documented history of deposits and maintaining a positive balance can sometimes help in the approval process for an initial credit card, particularly for those with a “thin file” (little to no U.S. credit history).

- 2026 Trend: Many institutions now use “Cash-Flow Underwriting,” meaning they may look at your bank account activity rather than just a traditional credit score to determine your eligibility.

Phase 2: The Strategic First Application (Days 8–15)

Once your identity is established, the next step is obtaining a “reporting trade line”—your first credit card.

Cross-Border Credit History

If you have a strong credit record in countries such as India, Mexico, Canada, Australia, or the UK, you may not have to start from zero.

- International Transfer Services: Companies like Nova Credit partner with lenders like American Express to “translate” your international credit report into a U.S. equivalent. This can potentially allow you to qualify for a high-tier card shortly after arrival.

- Professional Tip: Check if your home-country bank has a U.S. presence (e.g., HSBC), as they may offer “global transfer” services that carry over your internal bank standing.

Selecting Your First Card

For most students, the goal is an unsecured student card. However, if you are denied, a secured credit card—which requires a refundable security deposit—remains a highly effective and reliable tool for building history.

- Pre-Approval Tools: Always utilize “pre-approval” or “pre-qualification” links on bank websites. These use “soft inquiries” that do not affect your credit score, allowing you to see your odds of approval before committing to a formal application.

Phase 3: Mastering the Mechanics of FICO (Days 16–25)

The moment you receive your card, your behavior is being tracked. Understanding the mathematical components of your credit score can help you manage it more effectively.

| Factor | Weight | What It Means |

|---|---|---|

| Payment History | 35% | On-time payments vs. late payments |

| Credit Utilization | 30% | How much of your credit limit you use |

| Length of Credit History | 15% | Age of your credit accounts |

| Credit Mix | 10% | Types of credit (cards, loans, etc.) |

| New Credit / Inquiries | 10% | Recent credit applications |

Key Insight: In your first 6–12 months, only three factors truly matter: Payment History, Utilization, and New Credit. Focusing on these alone can produce a strong early score profile.

The First-Year Credit Rule = Consistency > Optimization

In your first 12 months, your goal is not to maximize rewards or apply for multiple cards. Your only objective is to build a clean, reliable credit profile. This means:

- Never miss a payment (0 late payments)

- Keep your credit utilization low (ideally under 10–30%)

- Limit new applications to avoid unnecessary hard inquiries

If you consistently follow these three rules, you can build a strong credit foundation without needing complex strategies.

Why this matters:

Most early credit damage happens when new users try to “optimize” too quickly. In reality, lenders reward stability and predictability far more than aggressive usage.

Note: Exact scoring models (such as FICO® Score 8 or FICO® Score 10) may vary slightly depending on the lender, but the overall weighting principles remain broadly consistent across the industry.

The Role of Credit Utilization

Credit utilization is the ratio of your outstanding balance to your total credit limit. It is one of the most significant factors in your score.

The Utilization Formula:

$$\text{Credit Utilization \%} = \left( \frac{\text{Total Credit Balance}}{\text{Total Credit Limit}} \right) \times 100$$

- Best Practice: While many sources suggest keeping utilization below 30%, industry data suggests that keeping it below 10% is often associated with the highest credit scores. If your limit is $500, try to ensure your reported balance is $50 or less.

The Necessity of On-Time Payments

Your payment history is generally considered the single most important factor in your credit score.

- Automation is Key: Set up “Autopay” for the Full Statement Balance every month. This ensures you avoid late fees and, more importantly, prevents 30-day late marks that can remain on your credit report for up to seven years.

- Zero Interest: By paying the statement balance in full each month, you avoid the high interest rates common with student cards, effectively using the card as a free financial tool.

Phase 4: Diversifying Your Profile (Days 26–30)

To move beyond a “thin file,” you can look at non-traditional reporting methods that add depth to your credit report.

Rent and Utility Reporting

For many international students, rent and utilities are their largest monthly expenses. Traditionally, these did not help your credit score, but that has changed.

- Reporting Services: Services like Bilt Rewards, Boom, or Experian Boost can report your on-time rent, phone, and utility payments to the bureaus.

- Potential Impact: A 2024 analysis by TransUnion indicated that consumers who had their rent payments reported to credit bureaus often saw an improvement in their scores, especially those starting with no prior history.

Strengthening Your “Credit Mix” (The Installment Hack)

While credit cards are a powerful starting point, the FICO® model rewards a diverse “Credit Mix,” which accounts for 10% of your total score. Lenders want to see that you can handle both revolving credit (cards) and installment credit (loans).

- As an international student, you likely aren’t ready for a car loan or a mortgage. To bridge this gap without needing a high U.S. income, consider a Credit Builder Loan (offered by providers like Self or SeedFi). These are specialized accounts where you “pay” a small monthly amount into a locked certificate of deposit (CD). The provider reports these on-time payments to the bureaus as installment loan history. Once the term ends, you receive your money back (minus a small fee), leaving you with a significantly “thicker” and more diverse credit profile.

What Results Should You Expect?

If you follow this 30-day plan consistently, a typical progression may look like:

- Month 1–2: Credit file established (no score yet)

- Month 3–6: Initial score generated (typically 650–700 range)

- Month 6–12: Score stabilizes and improves with consistency

- After 12 Months: Eligible for higher-limit cards, better loan rates

Important: Results vary based on usage patterns, payment behavior, and number of accounts.

Note on Interest Rates (APR): Student credit cards in 2026 typically carry a high Annual Percentage Rate (APR), often ranging from 19.24% to 29.99% Variable, depending on the prime rate and your individual creditworthiness. While these rates are high, they are essentially irrelevant if you follow the CCV 10/10/10 Rule and pay your Statement Balance in full every month. Interest is only charged when you “revolve” or carry a balance; by paying in full, you utilize the bank’s money for free while building your score.

Comprehensive Student Credit Card Comparison (2026)

Chase Freedom Rise℠ Student Credit Card

Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: Moderate (Requires $250 in a Chase checking account)

- Eligibility: F-1 or J-1 students with U.S. bank account, 18+ years old

- Why This Card is Best: This card is ideal for international students looking to establish long-term credit with a major U.S. bank. Chase’s ecosystem offers robust perks and future upgrade paths.

- Pros:

- Earn 1.5% cashback on all purchases.

- No annual fee for students.

- Automatic credit line increase after responsible use.

- Access to Chase’s extensive branch and ATM network.

- Cons:

- Requires maintaining $250 in a Chase checking account for better approval odds.

- Limited reward categories compared to other student cards.

- Credit Card Views / Rating: 9.8/10

- Perfect for building a strong U.S. credit history while gaining access to a major bank ecosystem.

Get Approved

Discover it® Student Credit Card

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: Low

- Eligibility: Students aged 18+ with proof of enrollment

- Why This Card is Best: Offers excellent cashback rewards and a forgiving first-year policy. Ideal for students who want rewards without high fees or complex requirements.

- Pros:

- 5% cashback on rotating categories each quarter (up to $1,500 in purchases).

- Unlimited 1% cashback on all other purchases.

- Cashback Match: Discover doubles all rewards earned in the first year.

- No late fee on first missed payment, making it forgiving for beginners.

- Cons:

- Less widely accepted internationally compared to Visa or Mastercard.

- Rotating categories may require attention to maximize rewards.

- Credit Card Views / Rating: 9.7/10

- Highly suitable for students who want cashback rewards and easy approval.

Get Approved

Capital One SavorOne Student Credit Card

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: Low to Moderate

- Eligibility: Students with proof of enrollment or regular income

- Why This Card is Best: Perfect for students who frequently spend on food, groceries, and streaming services. No foreign transaction fees make it ideal for international students.

- Pros:

- 3% cashback on dining, entertainment, and popular streaming services.

- 1% cashback on all other purchases.

- No foreign transaction fees for international usage.

- No annual fee for students.

- Cons:

- Rewards are not as broad as some flat-rate cashback cards.

- Moderate approval difficulty if student has limited banking history.

- Credit Card Views / Rating: 9.5/10

- Great for students seeking everyday spending rewards and international flexibility.

Get Approved

Deserve EDU Mastercard

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion

- Approval Difficulty: Very Low

- Eligibility: F-1 or J-1 students, no SSN required

- Why This Card is Best: Designed specifically for international students, it allows those without SSNs to get a card and start building credit immediately.

- Pros:

- No SSN required; ideal for newcomers.

- Includes 1-year Amazon Prime Student subscription.

- Can be approved even with limited U.S. financial history.

- No annual fee.

- Cons:

- Does not report to Equifax, meaning partial credit file coverage.

- Lower rewards compared to major banks.

- Credit Card Views / Rating: 9.2/10

- Excellent entry-level card for students just arriving in the U.S.

Get Approved

American Express Blue Cash Everyday® Card (Student Version)

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: High (Requires strong international credit history or banking references)

- Eligibility: Students with U.S. or verified international credit history

- Why This Card is Best: Ideal for students with established credit abroad, offering generous cashback on groceries, gas, and department stores.

- Pros:

- 3% cashback at U.S. supermarkets (up to $6,000 per year).

- 3% cashback on select streaming services.

- 1% cashback on other purchases.

- No annual fee.

- Cons:

- High approval difficulty for newcomers without U.S. credit.

- Limited acceptance in smaller stores outside major cities.

- Credit Card Views / Rating: 9.6/10

- Best for international students bringing credit history from their home country.

Get Approved

Zolve Azpire Credit Card

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: Low

- Eligibility: International students; can apply before arriving in the U.S.

- Why This Card is Best: Unique pre-arrival application allows students to start building U.S. credit even before reaching the country.

- Pros:

- No SSN required.

- Can be applied for from abroad.

- No annual fee.

- Reports to all 3 credit bureaus.

- Cons:

- Limited physical branch support; mostly online services.

- Relatively new brand with less widespread merchant familiarity.

- Credit Card Views / Rating: 8.9/10

- Ideal for students planning ahead and wanting to hit the ground running.

Get Approved

Petal® 2 Visa® Credit Card

- Annual Fee: $0

- Credit Bureau Reporting: Experian, TransUnion, Equifax (All 3)

- Approval Difficulty: Moderate

- Eligibility: Students and newcomers with proof of income or cash flow

- Why This Card is Best: Uses bank account data to evaluate creditworthiness, making it suitable for students with limited or no credit history.

- Pros:

- No annual fee.

- Reports to all 3 credit bureaus.

- Uses cash-flow underwriting instead of relying solely on FICO scores.

- 1%–1.5% cashback on purchases, increasing with responsible use.

- Cons:

- Moderate approval difficulty for students with irregular income.

- Rewards are modest compared to other cards.

- Credit Card Views / Rating: 9.1/10

- Best for students who want a data-driven, inclusive approach to building credit.

Expert Advice for Long-Term Success

On Inquiries: “Every ‘Hard Pull’ on your credit report can temporarily dip your score. During your first year, aim to apply for no more than two credit cards to maintain a clean record.” — Industry Consensus from National Credit Unions.

On Identity Matching: “Ensure your name and address are formatted identically across your lease, your bank account, and your credit card application. Discrepancies can lead to ‘split files,’ which can make it appear as though you have no credit when you actually do.” — Credit Reporting Best Practices.

The 5 Most Common Credit Mistakes International Students Make

- Applying for Too Many Cards Too Quickly: Multiple hard inquiries in a short time can signal risk to lenders.

- Maxing Out a Low Credit Limit: Even a $300 balance on a $500 card (60% utilization) can significantly lower your score.

- Missing the First Payment: A single missed payment early in your credit journey has a disproportionately large negative impact.

- Closing Their First Credit Card Too Early: Your oldest account strengthens your credit age—closing it can reduce your score.

- Ignoring Statements and Billing Cycles: Many students confuse “due date” with “statement closing date,” which affects utilization reporting.

Case Study: Rahul’s First 6 Months in the U.S.

Rahul, an F-1 student from India, arrived in the U.S. in August 2026 with no U.S. credit history. By following a structured 30-day credit plan, he was able to establish a strong financial foundation quickly. Here’s what he did:

Month 1 – Documentation & Banking

- Applied for an SSN through his university’s International Student Services office.

- Opened a checking account at a bank that offered student credit products.

- Maintained a small, steady balance to demonstrate financial responsibility.

Month 2 – First Credit Card

- Used a Nova Credit report to qualify for a Deserve EDU Mastercard without an SSN.

- Kept utilization under 10% and set up autopay for the full statement balance.

Months 3–4 – Consistency & Monitoring

- Paid all bills on time.

- Tracked credit progress using free tools.

- Avoided applying for multiple cards to prevent unnecessary hard inquiries.

Months 5–6 – Profile Diversification

- Signed up for a Credit Builder Loan from Self to add an installment account.

- Enrolled in Experian Boost to report on-time phone and utility payments.

Result After 6 Months

- Rahul’s credit file was fully established.

- His initial FICO score landed in the 680–700 range.

- He was approved for a higher-limit Chase Freedom Rise℠ card without difficulty.

- By maintaining responsible habits, Rahul set himself up for better loan rates, apartment rentals, and long-term financial success.

Takeaway: With a clear 30-day plan and disciplined habits, even students starting from zero can quickly establish a strong U.S. credit profile.

10 Essential FAQs for International Students

Do I need a job to get a student credit card?

Not necessarily. Lenders often allow you to list “personal income,” which can include stipends, scholarships, or allowances from parents.

How soon will I have a credit score?

It generally takes six months of activity for a FICO score to be generated, though some other scoring models (VantageScore) may appear sooner.

Will my foreign credit cards help my U.S. score?

Typically, no. U.S. credit bureaus are separate entities. Only specialized transfer services like Nova Credit can bridge that gap.

Is it okay to have a $0 balance?

It is better to have a very small balance (e.g., $5) report on your statement than $0, as it proves you are actively and responsibly using the credit.

Should I pay for “Credit Repair” services?

No. As a student starting with a clean slate, you do not need repair. You only need to build, which you can do yourself for free.

Does a debit card build credit?

No. Debit cards draw from your own funds and do not involve a line of credit; therefore, they are not reported to bureaus.

What happens to my score if I leave the U.S. after graduation?

Your score will remain on file for several years. If you return later, your history will still be there, though it may be considered “dormant.”

Can I get a credit card on a J-1 visa?

Yes. The process is virtually identical to that of an F-1 visa holder.

Why was my application denied even though I have money in the bank?

Lenders look at your history of repayment, not just your current balance. If you are denied, consider a secured card first.

How often should I check my credit report?

You can check it for free once a week at AnnualCreditReport.com. In your first year, checking once a month is usually sufficient.

The Credit Card “Pre-Flight” Checklist

Before you click “Apply,” ensure you have these 5 items ready to avoid a technical denial or an identity mismatch.

- The “Character-Perfect” Name: Your name on the application must match your Bank Account and Passport exactly. If your bank account says “Rahul S. Kumar,” do not apply as “Rahul Kumar.” Discrepancies lead to “Split Files” that are a nightmare to fix.

- Current U.S. Physical Address: Do not use a P.O. Box. Use your actual dorm or apartment address. Ensure you know the exact ZIP code and apartment number format used by the U.S. Postal Service.

- Total Annual Income: Remember, for credit applications, “Income” isn’t just a salary. You can legally include Scholarships, Grant Money, Stipends, and even allowances sent from parents, as long as you have reasonable access to those funds to pay your bill.

- Digital Copies of Documents: Have a PDF or clear photo of your Passport, F-1/J-1 Visa, and I-20 ready. Fintechs like Deserve or Zolve will often ask you to upload these immediately after you submit the form.

- A “Clean” Browser: Before applying, clear your browser cookies or use an Incognito/Private window. Sometimes, old tracking data can interfere with “Pre-Approval” tools or “Cashback Match” offers.

Final Tip: If the application asks for a “Social Security Number” and you don’t have one, look for a checkbox that says “I do not have an SSN” or “Use Passport/International ID.” Do not leave it blank unless instructed, as the system may auto-reject the form!

Conclusion

Establishing credit in a new country is a process that requires patience and discipline. While the initial lack of a score can be frustrating, following a structured 30-day plan—focusing on proper documentation, strategic card selection, and responsible utilization—can help you build a professional financial profile. By the time you complete your studies, your credit score can be a powerful asset rather than a barrier to your success.

Final Insight

In the United States, your credit score is more than just a number—it is a long-term record of your financial behavior. It can influence not only borrowing decisions, but also renting, insurance pricing, and even certain employment screenings.

Unlike academic results or one-time achievements, credit is built gradually and requires ongoing discipline. Students who understand this early are better positioned to avoid years of unnecessary financial friction and missed opportunities. Build it early, manage it wisely, and it will quietly open doors for years to come.

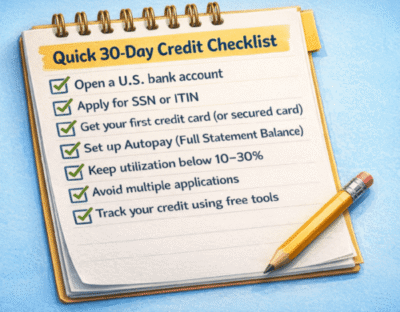

Quick 30-Day Credit Checklist

- [ ] Open a U.S. bank account

- [ ] Apply for SSN or ITIN

- [ ] Get your first credit card (or secured card)

- [ ] Set up Autopay (Full Statement Balance)

- [ ] Keep utilization below 10–30%

- [ ] Avoid multiple applications

- [ ] Track your credit using free tools

- [ ] Consider rent/utility reporting

-END-

About the Author – Alen Vi : Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer : The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure : CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.