Written by : Alen Vi | Creditcardviews.com

✅ [✓]Verification Badge: Market Data, APR Rates, and Policy Research Verified as of April 4, 2026.

The day you land at JFK, O’Hare, or LAX, your heart is full of a singular, electric hope. You’ve packed your life into four suitcases, said tearful goodbyes to the streets that raised you, and stepped into the unknown. But as the initial adrenaline of arrival fades, it is often replaced by a cold, sharp realization: The United States runs on a hidden currency called a Credit Score.

In 2026, the financial landscape for a new immigrant is more complex than ever. While the economy has stabilized after years of volatility, the “cost of entry” remains high. To rent an apartment, you need a deposit. To get to work, you need a car. To sleep comfortably, you need a bed. For someone with no U.S. credit history, these basic needs carry a “hidden tax” of high interest rates. Whether you are settling in high-cost hubs like San Francisco, California or fast-growing metros like Austin, Texas, these setup costs are unavoidable.

However, there is a path through the wilderness. By mastering the 21-month 0% APR credit card strategy, you can bypass the predatory interest rates that trap so many newcomers. This isn’t just about “saving money”—it’s about protecting your peace of mind and ensuring your American dream doesn’t start with a debt nightmare.

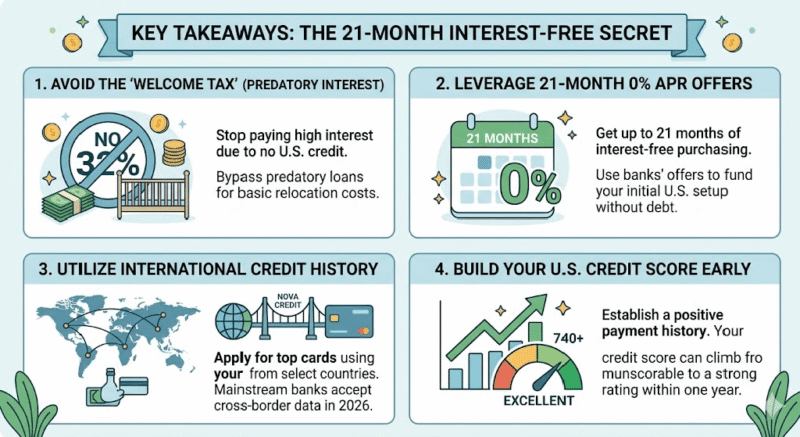

1.📊Why New US Immigrants Have No Credit Score (Credit Invisibility Explained)

👤 Real Story: Elena. She arrived from São Paulo in early 2026 with a Master’s degree, five years of banking experience, and a perfect credit record in Brazil. Yet, when she walked into a furniture store in Miami to buy a crib for her expected baby, she was declined. Not because she didn’t have money, but because in the eyes of the U.S. financial system, she didn’t exist.

“It felt like I was being erased,” Elena recalls. “I had worked so hard my whole life to be responsible, and suddenly, I was being treated like a risk. I ended up buying the crib on a store card with a 32% interest rate because I didn’t think I had a choice.”Elena’s story is the story of millions. According to a 2026 Consumer Financial Protection Bureau (CFPB) report, nearly 15% of the adult population in the U.S. is “credit invisible” or has an “unscorable” thin file. For immigrants, this percentage is drastically higher. This invisibility isn’t just a logistical hurdle; it is an emotional burden that creates a sense of “otherness” in a country where you are trying to belong.

💸The Financial “Welcome Tax” If Elena had financed $5,000 of basic household needs at that 32% interest rate, she would have paid over $1,600 in interest alone in just one year. This is the “Welcome Tax” that new immigrants pay simply for being new. The 21-month secret is designed to abolish that tax.

2.🔍Deciphering the 21-Month Secret: How It Works

The “secret” is a strategic alignment of two powerful forces: Introductory APR offers and Cross-border credit reporting. In 2026, several top-tier U.S. banks have extended their “introductory windows” to a staggering 21 months. This means for almost two years, the bank charges you zero interest on your purchases.

🧠 The Expert Perspective: Why 21 Months?

“Banks are in a fierce battle for the ‘New American’ demographic in 2026,” says Sarah Miller, Senior Analyst at the Financial Health Network. “By offering a 21-month interest-free runway, banks like Wells Fargo and Chase are essentially giving immigrants a zero-interest loan. Their goal is to win your loyalty so that when you’re ready for a mortgage in five years, you won’t look anywhere else.”

📈The Mathematical Miracle

Let’s look at the math for a typical relocation budget of $12,000 (covering a car down payment, first/last month’s rent assistance, and furniture)

| Strategy | Interest Rate (APR) | Monthly Payment | Total Interest Paid | Total Cost |

| ❌Predatory/Store Card | 31.99% | $754 | $3,834 | $15,834 |

| ⚠️Standard Credit Card | 19.58% | $680 | $2,280 | $14,280 |

| ✅The 21-Month Secret | 0.00% | $571 | $0 | $12,000 |

By using the 0% APR card, you save $2,280 compared to a standard card and a life-changing $3,834 compared to a store card. That is money that stays in your savings account, acting as your “American Safety Net.”

3.💳Top 7 Credit Cards for Immigrants in 2026

To help you navigate the sea of options, we have analyzed the current market. These cards are selected based on their introductory length, immigrant-friendly application processes, and overall value.

- 🏆Wells Fargo Reflect® Card

![]()

- The “Long-Haul” Champion

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 21 months from account opening on purchases and qualifying balance transfers.

- Eligibility: Good credit (670+). Tip: Use your international history via Nova Credit.

- Why it’s suitable: It provides the longest possible window to pay back relocation costs without a penny of interest.

- Pros: Cell phone protection (up to $600); No annual fee.

- Cons: No rewards or cash back.

- Expert Rating: ⭐⭐⭐⭐⭐ (9.8/10)

- 🏆Chase Slate®

![]()

- The “Reliable Foundation”

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 21 months on purchases and balance transfers.

- Eligibility: Chase has expanded its “Alternative Data” program in 2026, allowing immigrants to show bank account history instead of just a FICO score.

- Why it’s suitable: Chase is a “Big Three” bank. Building a relationship here opens doors to premium travel cards later.

- Pros: Access to Chase Credit Journey; High trust factor.

- Cons: Strict “5/24” rule (you can’t get this card if you’ve opened 5 cards in the last 24 months).

- Expert Rating: ⭐⭐⭐⭐⭐ (9.6/10)

- 🏆BankAmericard® Credit Card

![]()

- The “Account Holder’s Choice”

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 21 billing cycles.

- Eligibility: Highly accessible if you open a Bank of America checking account first.

- Why it’s suitable: Bank of America has a long history of serving the immigrant community and often accepts ITINs in lieu of SSNs.

- Pros: No penalty APR (missing a payment won’t automatically raise your interest rate).

- Cons: No rewards program.

- Expert Rating: ⭐⭐⭐⭐ (9.3/10)

- 🏆Citi® Simplicity® Card

![]()

- The “Stress-Free” Option

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 21 months on purchases.

- Eligibility: Moderate to Good credit.

- Why it’s suitable: Moving is stressful. This card removes the fear of “gotcha” fees.

- Pros: No late fees; No penalty APR; Ever.

- Cons: 5% balance transfer fee (higher than others).

- Expert Rating: ⭐⭐⭐⭐ (9.1/10)

- 🏆American Express Blue Cash Everyday®

![]()

- The “Daily Life” Multiplier

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 15 months.

- Eligibility: Excellent for Immigrants. Amex allows you to use your credit history from select countries (UK, India, Mexico, etc.) via their “Global Card Relationship” program.

- Why it’s suitable: While the 0% window is shorter (15 months), it rewards you for living.

- Pros: 3% Cash Back at U.S. supermarkets, online retail, and gas stations.

- Cons: Shorter interest-free window than the 21-month giants.

- Expert Rating: ⭐⭐⭐⭐ (8.9/10)

6.🏆Capital One Quicksilver Cash Rewards

![]()

- The “Simplicity” King

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 15 months.

- Eligibility: Fair to Good credit. Capital One is often the first “unsecured” card an immigrant can get.

- Why it’s suitable: It rewards every dollar spent, helping you recoup even more of your moving costs.

- Pros: Unlimited 1.5% cash back; No foreign transaction fees (great for visiting home).

- Cons: Higher interest rate after the 0% period ends.

- Expert Rating: ⭐⭐⭐⭐ (8.7/10)

- 🏆Discover it® Cash Back

![]()

- The “Human Touch” Card

- Fees: $0 Annual Fee.

- Introductory Offer: 0% Intro APR for 15 months.

- Eligibility: Very friendly to new-to-country applicants.

- Why it’s suitable: Their customer service is 100% U.S.-based and incredibly helpful for people navigating the system for the first time.

- Pros: Cashback Match at the end of the first year (doubles all your rewards).

- Cons: Not as widely accepted internationally as Visa/Mastercard.

- Expert Rating: ⭐⭐⭐⭐ (8.5/10)

4.📊 Real-World Case Study: The “Arjun Method”

Arjun moved from Bangalore to Chicago in January 2026 for a software engineering role. His salary was high, but his U.S. credit score was non-existent. He needed to furnish a two-bedroom apartment for his wife and daughter.

📊 INFOGRAPHIC SUMMARY: The Arjun Method (The $8k Interest-Free Roadmap)

- Total Purchases: $8,000 (Furniture, Tech, Home Goods)

- The Tool: 21-Month 0% APR Card

- The Monthly Payment: $400 (Targeted to finish in 20 months)

- The Savings: $1,600 (Money not paid to bank interest)

- The Result: 745 Credit Score within one year.

Arjun applied for the Wells Fargo Reflect® Card using the “International Credit” option. He was approved with a $10,000 limit and put the entire $8,000 on the card. By Month 20, Arjun had paid off the entire balance. He had paid $0 in interest. During that same period, his credit score climbed from “Unscorable” to 745.

“The card gave us a home,” Arjun says. “Without it, we would have been sleeping on air mattresses for six months while I saved up the cash. It allowed us to start our life with dignity.”

5.🌐The “Nova Credit” Revolution: Using Your Past to Fund Your Future

One of the most significant advancements in 2026 is the mainstream adoption of Cross-Border Credit Mapping. Today, companies like Nova Credit act as a bridge.

How it Works (Step-by-Step):

Selection: You apply for a U.S. credit card.

Consent: During the application, you check a box that says, “I have credit history outside the U.S.”

The Bridge: Nova Credit securely pulls your report from your home country’s bureau.

Translation: They translate that data into a U.S.-equivalent score.

Instant Approval: The U.S. bank uses that score to approve you for a high-limit, 0% APR card immediately

6.🧠Pro-Tips: Secrets the Banks Won’t Tell You

- The “Utilization” Ghost: If you use 90% of your credit limit, your credit score will drop. Secret: If you need to spend $5,000 but your limit is $5,000, try to pay off $1,000 immediately so the “reported” balance is only 80%.

- The “Statement Date” vs. “Due Date”: Banks report your balance to the credit bureaus on the statement date, not the due date. To keep your score high, pay your monthly portion a few days before the statement closes.

- The “Double Play”: One spouse gets a 21-month card now. In 12 months, the other gets one. This gives your family an interest-free window that lasts nearly three years.

- Watch the “Minimum Payment” Trap: The bank will only ask for a minimum payment (usually around $25–$50). If you only pay the minimum, you will still owe thousands when the 21 months are up. Always divide your total balance by 20.

- The “Soft Pull” Check: Use the “Pre-Approval” tools on the Wells Fargo or Capital One websites first. These “Soft Pulls” don’t hurt your score but tell you if you’re likely to be accepted.

7.⚖️ Comparison Chart: 0% APR vs. Other Funding Options

| Feature | 21-Month 0% APR Card | Personal Loan | Secured Credit Card | Store Finance (Deferred) |

| Cost of Borrowing | $0 | 9.5% – 18% | $0 (requires deposit) | $0 (IF paid in full) |

| Credit Building | Excellent | Good | Moderate | Poor |

| Flexibility | High (spend anywhere) | Moderate (lump sum) | Low (tiny limits) | Very Low (one store) |

| Risk Level | Low (if disciplined) | Moderate | Very Low | High (Interest Traps) |

8.🏆 Expert Advice: The 3 Pillars of Immigrant Financial Success

Dr. Linda Rodriguez, Director of the New American Financial Initiative

- , shares her rules for 2026 arrivals:

- Pillar 1: Protect the 0% Window. Set up ‘Autopay’ the very first day.

- Pillar 2: Avoid ‘Lifestyle Creep’. Use the 0% only for ‘Investment Purchases’—things that help you earn money or save money.

- Pillar 3: Diversify Your Credit. Consider adding a small ‘Credit Builder Loan’ of $500 to show you can handle different types of debt.

9. ⚠️Common Pitfalls: Why 0% APR Can Be Dangerous

- The “Cliff” Effect: On the 22nd month, your interest rate might jump from 0% to 28.99%. If you still owe $5,000, you will suddenly be charged $120 per month just in interest.

- The “Deferred Interest” Scam: Some store cards charge interest on the full original amount if you have $1 left on the balance at the end of the term. The cards we listed do NOT do this. * Balance Transfer Fees: If you use the card to pay off another debt, you will likely pay a 3% to 5% fee.

10.❓Frequently Asked Questions (FAQ)

Q1: Can I get these cards if I only have an ITIN and no SSN?

Yes. Bank of America and American Express are known for accepting ITINs.

Q2: What is the minimum credit score needed?

Generally, 670+, but international history via Nova Credit bypasses the need for a U.S. score.

Q3: Does 0% APR apply to cash withdrawals?

No. Cash advances carry immediate 25%+ interest rates.

Q4: Will my credit score drop if I close the card after 21 months?

Yes. Keep the card open, but stop using it to maintain your “length of credit history.”

Q5: Can I use these cards to pay my rent?

You can via platforms like Plastiq, though a 2.9% fee usually applies.

Q6: What if I lose my job?

Contact the bank immediately for “Hardship Programs” available in 2026.

Q7: Is it better to get one 21-month card or two 15-month cards?

One 21-month card is better for your credit score.

Q8: Can I use my 0% card back in my home country?

If it has “No Foreign Transaction Fees,” yes!

Q9: How do I know when my 21 months are up?

It will be on your monthly statement under “Promotional Summary.”

Q10: Does this work for international students?

Yes, though student 0% windows are usually 6–12 months.

11. 🏁Final Thoughts: Building a Legacy

The first 21 months in the United States are the most critical. By using the 21-Month Interest-Free Secret, you are refusing to be a “risk” and choosing to be a “strategist.” Remember Elena? She eventually used a Chase Slate card to pay for her daughter’s daycare. “The second time, I was in control,” she says. “I felt like an American who knew how to make the system work for her.”

You have already done the hardest part—you moved across the world. Managing a credit card is simple by comparison. Use these 21 months to build your home, build your score, and build the life you came here to live.

📚Research Sources & Citations:

- Federal Reserve Bank of New York: Quarterly Report on Household Debt (Q1 2026).

- Consumer Financial Protection Bureau (CFPB): “Credit Invisibility” Special Report 2026.

- Nova Credit: Global Credit Data Index 2026.

- Bankrate & J.D. Power: 2026 Credit Satisfaction Studies.

Disclaimer: This article is for informational purposes only. Credit card terms are subject to change by the issuing banks.

-END-

About the Author

Alen Vi : Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer : The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content. credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure : CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.