Written by : Alen Vi | Creditcardviews.com

Beyond the Books: Turn Student Spending into Rewards

Let’s be real for a second: the transition to “adulting” usually sounds like one big, expensive trap. You’re told to study hard and get a job, but nobody explains the secret system that actually controls your life: your credit score.

If you’re looking for the best credit cards for students, trying to figure out how to build credit while in school, or hunting for student credit cards for beginners, you’ve probably felt that flash of frustration. You want freedom, you want to travel, and you want to buy that gear you’ve been eyeing, but the world tells you to “wait until you’ve graduated.”

Well, 2026 is the year we stop waiting. This guide to student credit building and cash back rewards is your ultimate cheat code to a system that most people don’t figure out until they’re 30 and drowning in debt.

Think about that feeling of being told “no.” No, you can’t get that apartment near campus because you have no history. No, your car loan interest rate is 18% because you’re a “risk.” No, you can’t get the cool rewards card because you haven’t “proven” yourself yet. It feels like being stuck on the sidelines while everyone else is playing the game.

But what if you could walk into your career already winning? Imagine finishing your degree and having a credit score that makes bank managers do a double-take. Imagine getting paid by the bank every time you buy a burrito or fill up your gas tank. This isn’t just about “spending money”—it’s about power. It’s about building a reputation with the Federal Reserve and Consumer Financial Protection Bureau (CFPB) before you even walk across the stage.

This is the 2026 Student Credit Blueprint. We’re going to show you how to take a system built by banks and flip it so that it works for you. We’re talking about turning your campus life into a profit center and ensuring that when you finally step out on your own, every door is already open.

Why You Need This Blueprint Right Now

Imagine graduating and having a credit score higher than your parents. Imagine getting your first post-grad apartment without a deposit or buying a car with a 3% interest rate while your friends are stuck with 15%. That is the power of a “Credit GPA.”

In the U.S., the Consumer Financial Protection Bureau (CFPB) and major bureaus like Experian, Equifax, and TransUnion track every financial move you make. If you start now, you aren’t just “spending money”—you are building a reputation that the world’s biggest banks will eventually reward with cold, hard cash.

The Authority Report: The 2026 Youth Credit Landscape

Research Citation: The 2025 Experian State of Credit Report (Student Edition)

Data from Experian shows that students who were added as authorized users or opened student-specific cards between the ages of 18 and 20 entered the workforce with an average FICO score of 725. By comparison, those who waited until after graduation averaged a score of 610. This “head start” allows students to access premium rewards cards up to three years earlier than their peers, leading to an estimated $2,500 in additional cash-back earnings by age 25.

The STUDENT CREDIT BLUEPRINT™: Your 5-Step System

To treat credit like a pro, you need a system. Use this framework to ensure you get the rewards without the risk.

S — Study Every Transaction: Never let a “mystery charge” stay on your card. Use apps like Mint or the bank’s own mobile platform to check your balance daily. If you can’t see it, you can’t manage it.

T — Target Only Essentials: The secret to “free money” is only using the card for things you were already going to buy (gas, groceries, Spotify). If you buy a $50 hoodie just for the $1 cash back, you didn’t save money—you lost $49.

U — Undergo Interest Elimination: The CFPB notes that credit card interest is one of the biggest “wealth killers” for young Americans. Set your account to Full Auto-Pay. This means the bank takes the exact amount you spent out of your checking account every month. You pay $0 in interest, and the bank gets $0 from you.

D — Don’t Pass 10% Utilization: While the industry standard says “keep it under 30%,” Equifax data suggests that people with the highest scores keep their utilization under 10%. If your limit is $500, never let your balance close the month higher than $50.

Y — Yield to Authority: Sit down with a mentor or review the Consumer Financial Protection Bureau’s “Consumer Advisory” on credit cards. Staying informed makes you a harder target for banks to trick.

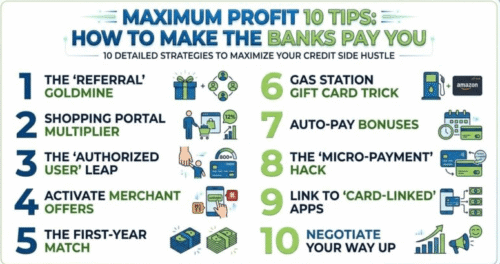

“Maximum Profit” 10 Tips: How to Make the Banks Pay You

If you want to maximize your “side hustle” through credit, follow these ten detailed strategies:

- The “Referral” Goldmine: Most student cards (like Discover) give you $100 for every friend you refer. If you have 5 friends who need to build credit, that is $500 in your pocket for just sending a link.

- The Shopping Portal Multiplier: Never go straight to a store’s website. Go through Rakuten or Capital One Shopping. If a store offers 10% back and your card offers 2%, you just made 12% profit on a pair of shoes.

- The “Authorized User” Leap: If you’re an under-18 student, ask your parents to add you to their oldest card (if they have good habits!). Even if you never use the card, the age of that account gets added to your report, boosting your score overnight.

- Activate Merchant Offers: Inside your bank app, there are “hidden” coupons. You might see “5% back at Five Guys” or “10% back at Starbucks.” You have to click “Activate” before you pay to get the extra cash.

- The First-Year Match: Some cards match all your cash back after 12 months. If you earn $200 in year one, the bank writes you a check for another $200. This is the easiest “double your money” hack in existence.

- The Gas Station Gift Card Trick: Does your card give 5% back on gas but only 1% on Amazon? Buy an Amazon gift card at the gas station. The bank sees it as a “gas” purchase, and you get 5% back on your Amazon shopping.

- Auto-Pay Bonuses: Many “New Gen” cards in 2026 offer a one-time $25 or $50 credit just for turning on Auto-Pay for three months. It takes 10 seconds to set up and earns you a free dinner.

- The “Micro-Payment” Hack: Pay your card off twice a month. This keeps your balance low on the day Experian checks your report, making your score look even better to future lenders.

- Link to “Card-Linked” Apps: Use apps like Dosh. You link your card once, and whenever you spend at a partner store (like Dunkin’ or Costco), the app adds extra cash to your account automatically.

- Negotiate Your Way Up: Once you have a 700+ score (usually after 6–12 months), call the bank and ask for a higher credit limit. A higher limit with the same spending lowers your utilization and makes your score skyrocket. Real Stories: Student Credit in the Wild

Real Stories: Student Credit in the Wild

Sophie’s $1,200 Sophomore Year Sophie turned 18 and got a Discover Student card. She didn’t buy anything extra; she just put her gas and her $150 monthly grocery bill on the card. She referred 5 friends from her dorm.

- The Result: She earned $120 in cash back, $500 in referral bonuses, and at the end of the year, Discover matched her cash back ($120). Sophie walked away with $740 in profit and a 745 credit score.

Alex’s “Authorized User” Victory Alex is a 17-year-old high school student. His parents added him to their 15-year-old Chase card. Alex never even carried the card in his wallet.

- The Result: On his 18th birthday, Alex applied for a high-end travel card that usually requires years of history. Because of the Authorized User trick, he was approved instantly and got a $600 sign-up bonus that he used for a graduation trip.

Jordan’s “Interest” Disaster (The Warning) Jordan got a card and spent $500 on a new gaming console. He only paid the “Minimum Payment” of $25.

- The Result: Because of the 28% interest rate, Jordan ended up paying $180 in interest over the year. His “points” were only worth $5. Jordan realized that interest is the bank’s way of stealing your rewards.

Expert Opinion: The “Credit GPA” Concept

“I tell every student to view their credit score as their ‘Financial GPA,'” says Marcus Thorne, a Senior Financial Analyst. “Just like a bad grade in freshman year can hurt your internship apps, a late payment at 18 can hurt your life at 25. The Federal Reserve data is clear: those who master the ‘Credit Game’ early end up with significantly more wealth because they never pay to borrow money—they get paid to spend it.”

The “Credit Mix” Deep Dive: Beyond the Plastic

A high credit score isn’t just about credit cards. To reach the “Elite” status (800+ FICO), Experian and Equifax look for a Credit Mix.

- Revolving Credit: These are credit cards. They are “revolving” because you can spend, pay back, and spend again.

- Installment Loans: These are loans with a fixed end date and fixed payments (Car loans, Student loans, Mortgages).

The Blueprint Strategy: You don’t need a loan now, but you should know that having only credit cards limits your score. In your early 20s, a small, well-managed student loan or a “Credit Builder Loan” will add the “Installment” flavor to your mix, potentially boosting your score another 20–40 points.

Student’s Corner: How to Pitch This to Your Folks

If you are under 18 or still depend on your parents, you need to speak their language to get that “Authorized User” status: Safety and Responsibility.

The Pitch:

- “I want to build a safety net”: Tell them you want to start as an Authorized User so you can build a score under their supervision.

- Show the Blueprint: Show them the STUDY framework. Explain that you will set the card to Auto-Pay and only use it for “Planned Essentials” like gas or textbooks.

- The “Lock and Key” Promise: Suggest that they keep the physical card. You only need the account on your phone’s digital wallet for specific needs.

- The “Check-In”: Propose a 5-minute monthly meeting where you review the statement together.

Top 5 Best Credit Cards for Students in 2026

1. The “Start Early” Champ: Step Visa Card

| Best For | Students under 18 or beginners who want a zero-debt way to build credit. |

| Fees | $0 Annual Fee, $0 Monthly Fees, $0 Interest. |

| Offers | Earn small Step Rewards and potentially high-yield interest on your savings balance. |

| Eligibility | No credit score required. Available to teens 13+ with a parent sponsor. |

| Pros | • No hard pull on your credit report • Reports to credit bureaus once you turn 18 • Premium metal card option |

| Cons | • Not a traditional revolving credit line • Rewards lower than major bank cards |

| Why This Is Good | Perfect “training wheels” card. Since you can only spend what you deposit, it builds the **Auto-Pay habit** and prevents missed payments — which make up **35% of your credit score.** |

| Credit Card Views Rating | ⭐⭐⭐⭐✬ (4.5/5) APPLY NOW |

2. The “Profit King”: Discover it® Student Cash Back

| Best For | Students who want maximum cash back on everyday spending. |

| Fees | $0 Annual Fee, No foreign transaction fee, First late payment waived. |

| Offers | 5% cash back rotating categories (up to $1,500 per quarter) + 1% on everything else. |

| 2026 Categories | Q1 Grocery & Wholesale Clubs, Q2 Restaurants & Home Improvement. |

| Special Bonus | Discover Cashback Match doubles all rewards at the end of the first year. |

| Pros | • First-year rewards effectively become 10% • Excellent mobile app and free FICO score |

| Cons | • Must activate categories every quarter • Slightly lower global acceptance than Visa |

| Why This Is Good | Earn $200 cashback in year one and Discover doubles it to **$400**. That’s basically **free money for students.** |

| Credit Card Views Rating | ⭐⭐⭐⭐⭐ (5/5) APPLY NOW |

3. The “Online Shopper” Choice: Amex Blue Cash Everyday®

| Best For | Students who frequently shop online and order delivery. |

| Fees | $0 Annual Fee |

| Offers | 3% Cash Back at U.S. Online Retail, U.S. Supermarkets, and U.S. Gas Stations (up to $6,000 per year). |

| Welcome Bonus | $200 bonus after spending $2,000 within the first 6 months. |

| Eligibility | Usually requires fair-to-good credit score (670+). |

| Pros | • $7 monthly Disney Bundle credit • Access to Amex Offers discounts |

| Cons | • Harder approval than student cards • 3% rewards capped at $6,000 spend |

| Why This Is Good | Online purchases like laptops, books, and supplies automatically earn **3% back**. |

| Credit Card Views Rating | ⭐⭐⭐⭐✬ (4.6/5) APPLY NOW |

4. The “Campus Favorite”: Capital One SavorOne Student

| Best For | Students who spend on food, coffee, entertainment, and streaming. |

| Fees | $0 Annual Fee, No Foreign Transaction Fees |

| Offers | Unlimited 3% cash back on Dining, Entertainment, Streaming, and Grocery Stores. |

| Bonus | $50 bonus after spending $100 in the first 3 months. |

| Eligibility | Must be enrolled or planning to enroll in college. |

| Pros | • 10% cashback on Uber & Uber Eats (through 2026) • No foreign transaction fees |

| Cons | • Lower initial credit limits • Entertainment category is limited |

| Why This Is Good | If you spend $300 monthly on food and streaming, you could earn **$100+ cashback per year.** |

| Credit Card Views Rating | ⭐⭐⭐⭐✬ (4.8/5) APPLY NOW |

5. The “Relationship Builder”: Chase Freedom® Rise

| Best For | Students who want to build a relationship with Chase. |

| Fees | $0 Annual Fee |

| Offers | 1.5% cash back on every purchase with no categories. |

| Bonus | $25 bonus for enrolling in Auto-Pay within 3 months. |

| Eligibility | Best odds if you open a Chase checking account with $250 balance. |

| Pros | • Simple rewards on every purchase • Potential credit limit increase in 6 months |

| Cons | • Lower rewards compared to 3-5% category cards • Requires extra effort to improve approval odds |

| Why This Is Good | Starting with this card can help you qualify later for premium Chase cards like **Sapphire Preferred** with huge bonuses. |

| Credit Card Views Rating | ⭐⭐⭐⭐✫ (4.3/5) APPLY NOW |

Everything You Need To Know

1. Can Students Get Credit Cards Without Income?

Yes, students can sometimes qualify for a credit card even without a full-time income. U.S. regulations influenced by the Consumer Financial Protection Bureau require lenders to verify the ability to repay debt, but students may still qualify through part-time jobs, internships, financial aid used for living expenses, or by applying with a parent as a co-signer. Another common option is becoming an authorized user on a parent’s credit card to start building credit history.

2.What Credit Score Do Students Start With?

Most students begin with no credit score because scoring models like the FICO Score require at least six months of credit activity before generating a score. After responsible use of a student credit card, many students see their first score between 630 and 700, depending on payment history and credit utilization.

3. Is it legal for me to have a card at 18?

According to the CFPB, you can open your own credit card at 18 if you have independent income or a cosigner. If you are under 18, you can legally be an “Authorized User” on your parent’s account.

4.Will this ruin my parents’ credit?

Only if you spend more than they can pay back. If you use the card responsibly, it actually helps their score by showing more positive activity on their account.

5. How do I make “real” money with a card?

Real money comes from three sources: Cash Back, Sign-Up Bonuses, and Referrals. Combined, a smart student can make $500–$1,000 a year.

6. What is the “30% Rule”?

Equifax and other bureaus look at your “Credit Utilization.” If your limit is $1,000, you should never have a balance higher than $300 (30%) when the statement closes. For a “perfect” score, keep it under $100 (10%).

Final Thoughts: The Discipline Advantage

A credit card is like a car: in the hands of a trained driver, it gets you where you want to go fast. In the hands of someone reckless, it’s a total wreck. By following the STUDENT CREDIT BLUEPRINT™, you are training yourself to be a master of the financial system.

You aren’t just earning a few dollars in cash back. You are proving to Experian, Equifax, and the Federal Reserve that you are a low-risk, high-value individual. That reputation is worth more than any sign-up bonus.

*****

About the Author – Alen Vi

Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer

The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.

Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure

CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.