Written by : Alen vi

Edited by : Credit card views Desk

Earn More Cash Back Every Day

Managing your money efficiently is easier with the right tools. No annual fee credit cards are an excellent way to save while earning cash back on your everyday purchases. With a smart strategy, every dollar spent can work harder for you.

Whether you’re shopping for groceries, filling up your gas tank, or paying for daily expenses, selecting the right cards and tracking your spending can significantly boost your rewards. This guide explains how to get the most cash back on groceries, gas, and everyday spending with no-fee U.S. cards.

Why No-Fee Cash Back Credit Cards Matter

No annual fee cards save you money from the start. While some premium cards offer rewards, paying yearly fees can offset your earnings. By sticking to no-fee cards:

- Every cash back dollar is profit.

- You can diversify cards without worrying about extra costs.

- Cancelling or switching cards doesn’t cost you money.

Additionally, cash back rewards programs allow you to earn back a percentage of your purchases automatically. With some cards offering higher rewards on groceries or gas, planning your spending can lead to substantial savings.

Understanding Cash Back Rewards

What Are Cash Back Rewards Programs?

Cash back programs give a percentage of your purchases back, usually as a statement credit or direct deposit. Some programs focus on specific categories:

- Groceries: Earn more when shopping at U.S. supermarkets.

- Gas: Rewards for fueling up.

- Dining & Everyday Purchases: Bonuses for restaurants or all other purchases.

How Cash Back Percentages Work

- Flat-rate cards: Earn a consistent percentage on all purchases.

- Category-specific cards: Earn higher percentages in selected categories.

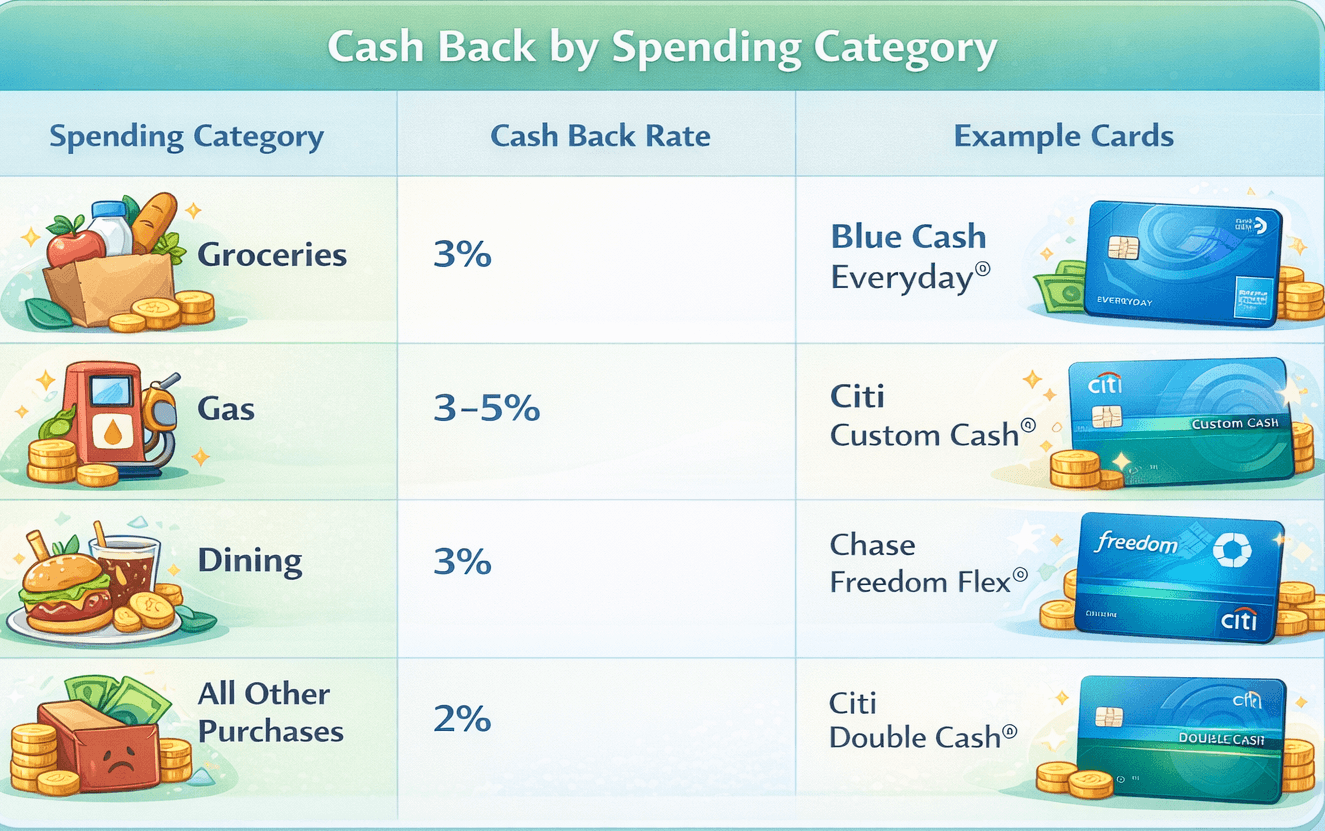

Top No-Fee Cash Back Cards for Groceries

Blue Cash Everyday Card from American Express

- 3% cash back at U.S. supermarkets (up to $6,000 per year, then 1%)

- 3% cash back at U.S. gas stations (up to $6,000 per year, then 1%)

- 3% cash back on U.S. online retail purchases (up to $6,000 per year, then 1%)

- 1% on other purchases

- $0 annual fee

Pros: Strong 3% categories, covers gas + groceries + online shopping, no annual fee.

Cons: $6,000 annual cap per category, 1% base rate outside bonus categories.

Welcome Offer: Typically $200 statement credit after qualifying spend.

Eligibility: Good to excellent credit (670+), U.S. resident, subject to Amex application rules.

Credit Card Views Rating: ☆ (4.5/5)

Chase Freedom Flex

- 5% cash back on rotating quarterly categories (up to $1,500 per quarter, activation required)

- 5% on travel through Chase Travel℠

- 3% on dining & drugstores

- 1% on all other purchases

- $0 annual fee

Pros: High 5% quarterly rewards, strong dining rewards, flexible Ultimate Rewards points.

Cons: Must activate categories quarterly, $1,500 quarterly cap.

Welcome Offer: Typically $200 bonus after minimum spend requirement.

Eligibility: Good to excellent credit, subject to Chase 5/24 rule.

Credit Card Views Rating: ☆ (4.6/5)

Citi Custom Cash Card

- 5% cash back on highest eligible spending category each billing cycle (up to $500 per month, then 1%)

- 1% on all other purchases

- $0 annual fee

Pros: Automatically adjusts to your top spending category, great for groceries or gas, no activation required.

Cons: $500 monthly cap, only one 5% category per cycle.

Welcome Offer: Typically $200 bonus after qualifying spend.

Eligibility: Good to excellent credit, U.S. applicants.

Credit Card Views Rating: ☆ (4.4/5)

Best Gas Rewards Cards Without Annual Fees

Bank of America Customized Cash Rewards Credit Card

- 3% cash back in chosen category (gas is an option)

- 2% at grocery stores & wholesale clubs

- 1% on other purchases

- 3% & 2% categories capped at $2,500 per quarter (combined)

- $0 annual fee

Pros: Choose your 3% category, strong grocery + gas combo, higher rewards for Preferred Rewards members.

Cons: Quarterly spending cap, base rate only 1%.

Welcome Offer: Typically $200 online bonus after qualifying spend.

Eligibility: Good credit recommended.

Credit Card Views Rating: ☆ (4.3/5)

Citi Double Cash Card

- 2% unlimited cash back (1% when you buy + 1% when you pay)

- $0 annual fee

Pros: Simple 2% flat rate, no caps, ideal companion card.

Cons: No bonus categories, must pay balance to earn full 2%.

Welcome Offer: Occasional $200 bonus after qualifying spend.

Eligibility: Good to excellent credit.

Credit Card Views Rating: ☆ (4.7/5)

Costco Anywhere Visa Card by Citi

- 4% on gas (up to $7,000/year)

- 3% restaurants & travel

- 2% at Costco

- 1% other purchases

- $0 annual fee (Costco membership required)

Credit Card Views Rating: ☆ (4.2/5)

Multi-Card Strategy for Maximum Returns

Best 3-card combo example:

- Groceries & Online: Blue Cash Everyday (3%)

- Gas: Citi Custom Cash (5%)

- Everything else: Citi Double Cash (2%)

This layered strategy can generate $400–$800+ annually depending on spending habits.

Understanding Rotating Categories

Quarterly examples may include:

- Q1: Gas – 5%

- Q2: Groceries – 5%

- Q3: Restaurants – 5%

- Q4: Online shopping – 5%

Always activate bonuses in your card’s app.

Grocery Shopping Strategies

- Supermarkets typically qualify (Kroger, Whole Foods).

- Superstores (Walmart, Target) may not qualify under supermarket categories.

- Buying gift cards at grocery stores can multiply rewards.

- Warehouse clubs may require specific cards like Costco Visa.

Gas Station Reward Strategies

- Combine credit card rewards with gas loyalty programs.

- Track spending caps.

- Use 5% category cards when gas qualifies.

Industry & Consumer Insights on Cash Back Rewards

Adding research and survey data boosts authority and helps readers understand real-world outcomes:

- Average cash back earned per cardholder: ~$250 per year across all cards.

Source: Zipdo – Credit Card Statistics - Base cash back rate: ~1.17% on purchases; category bonuses can increase this significantly.

Source: WalletHub – Average Cash Back Rates - Sign-up bonuses: Average $230–$250 per card.

Source: WalletHub – Credit Card Landscape Report - Total rewards earned nationally: In 2024, U.S. consumers earned ~$47.5 billion in rewards; cash back accounted for more than one-third.

Source: CFPB – Consumer Credit Card Market Report - Usage patterns:

- 58% of cardholders primarily use cash back cards.

Source: Digital Transactions – J.D. Power Survey - 71% of cardholders have unused rewards ($100+).

Source: LendingTree – Unused Rewards Study - 61% redeemed rewards for cash back or gift cards, 23% did not redeem at all.

Source: Bankrate – Credit Card Rewards Survey

- 58% of cardholders primarily use cash back cards.

Key Takeaway: Using cards strategically maximizes rewards, while failing to track or redeem them leads to missed opportunities.

Avoiding Common Mistakes

Tracking & Redeeming Rewards

- Use issuer apps to track category bonuses.

- Redeem as statement credits or direct deposits.

- Don’t let rewards sit unused.

- Pay balances in full monthly.

FAQs

Use a layered approach. Pair Blue Cash Everyday Card from American Express (3% at supermarkets) with a 2% flat-rate card like Citi Double Cash Card for non-bonus purchases.

Citi Custom Cash Card offers 5% on gas if it’s your top category (up to $500 per billing cycle).

Every reward dollar stays in your pocket, and you can build a multi-card setup without paying yearly fees.

Usually not under “U.S. supermarket” categories. Use a 2% flat-rate card for those purchases.

Cards like Chase Freedom Flex offer 5% quarterly bonuses. Activating and planning purchases during these periods maximizes earnings.

Most of these cards require good to excellent credit (typically 670+).

No. Always pay in full. Interest charges will exceed any rewards earned.

With a proper 2–3 card strategy, many households can earn $400–$800+ annually depending on spending levels.

Conclusion

Earning maximum cash back comes down to strategy:

- Know your spending patterns.

- Choose no-fee cards with strong bonus categories.

- Pair 5% category cards with 2% flat-rate cards.

- Track caps and activate rotating bonuses.

- Pay balances in full every month.

Top Picks Summary

- Groceries: Blue Cash Everyday®, Citi Custom Cash®

- Gas: Bank of America Customized Cash, Citi Custom Cash®

- Everyday Spending: Citi Double Cash®, Chase Freedom Flex®

By combining the right no-annual-fee credit cards and managing them wisely, you can turn everyday expenses into meaningful yearly cash back — without paying a single dollar in annual fees.

***********

About the Author – Alen Vi

Alen Vi is a seasoned financial expert with over 10 years of experience specializing in the credit card industry. Throughout his career, he has worked with various leading media firms, providing in-depth analysis, insights, and guidance on personal finance, credit card rewards, and smart spending strategies. At Credit Card Views, Alen combines his extensive knowledge and practical expertise to help readers make informed decisions, maximize their cash back and rewards, and navigate the complex world of credit cards with confidence.

Disclaimer

The information provided on Credit Card Views is for general informational and educational purposes only and is not intended as financial, legal, or professional advice. While we strive to provide accurate and up-to-date information about credit cards, rewards programs, fees, and offers, terms and conditions can change frequently, and we cannot guarantee the accuracy, completeness, or timeliness of all content.

Credit card offers and eligibility criteria vary by issuer, credit score, and individual circumstances. Before applying for any credit card or making financial decisions, readers should conduct their own research and consider consulting with a qualified financial advisor.

Trust & Affiliate Disclosure

CreditCardViews.com provides independent and expert guidance to help you make informed credit card and financial decisions. Some links on this site are affiliate links. If you make a purchase through them, we may receive a small commission at no extra cost to you. Our recommendations are always based on research, user feedback, and expert analysis, and are not influenced by our partners. CreditCardViews.com does not issue credit cards or provide financial products directly. Final approval decisions are made solely by the issuing banks. Your trust and financial well-being are our top priority. Our platform uses SSL encryption and follows FTC, GDPR, and CCPA standards to provide secure, unbiased, and transparent credit card insights.